The datasets, tested

against real prices.

Each Alphanume dataset focuses on a specific, tradable market effect. Here's every one of those claims, run against real prices, benchmarked to SPY, and put through real significance tests.

Every dataset, its headline result, and an honest verdict.

- 01

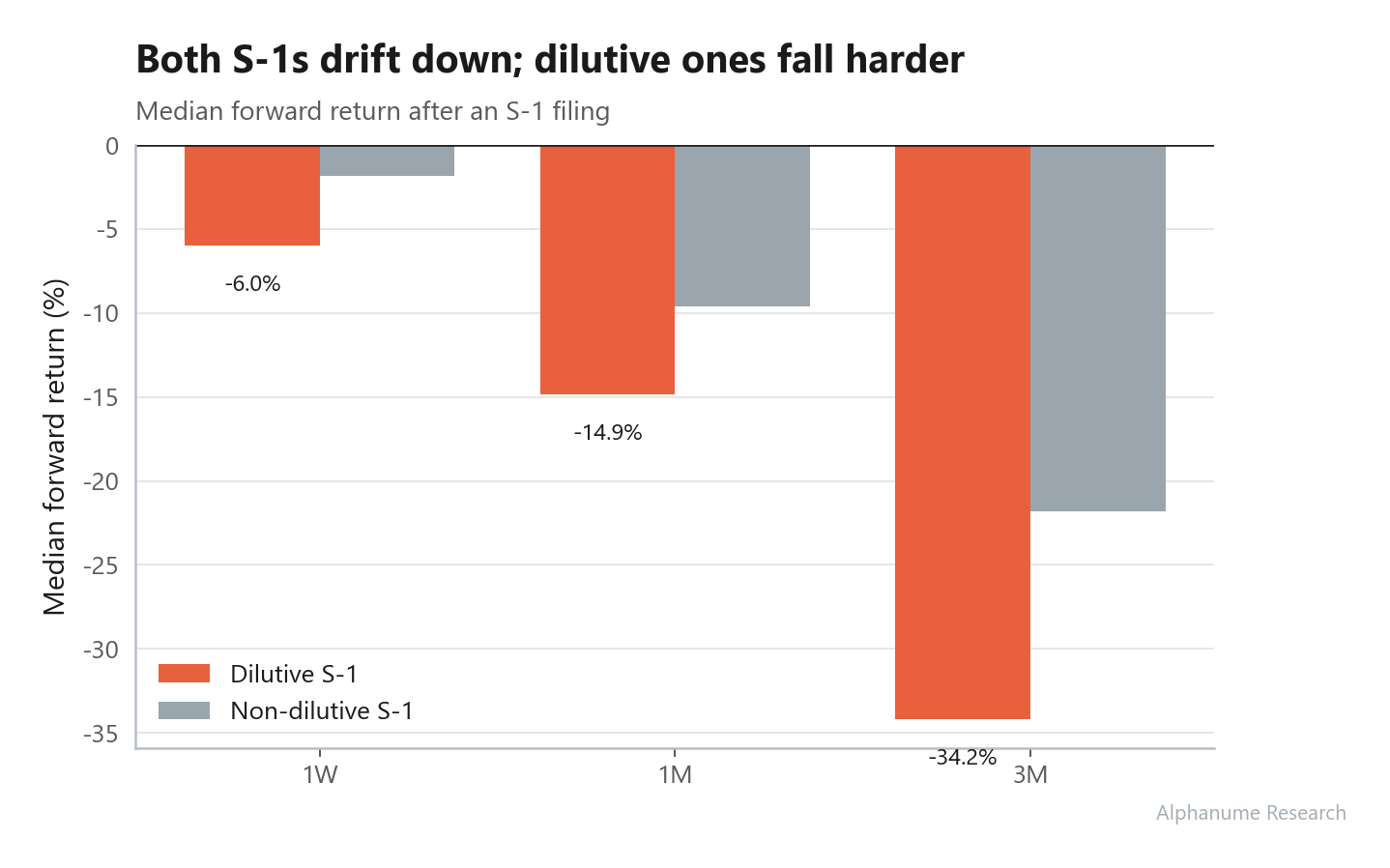

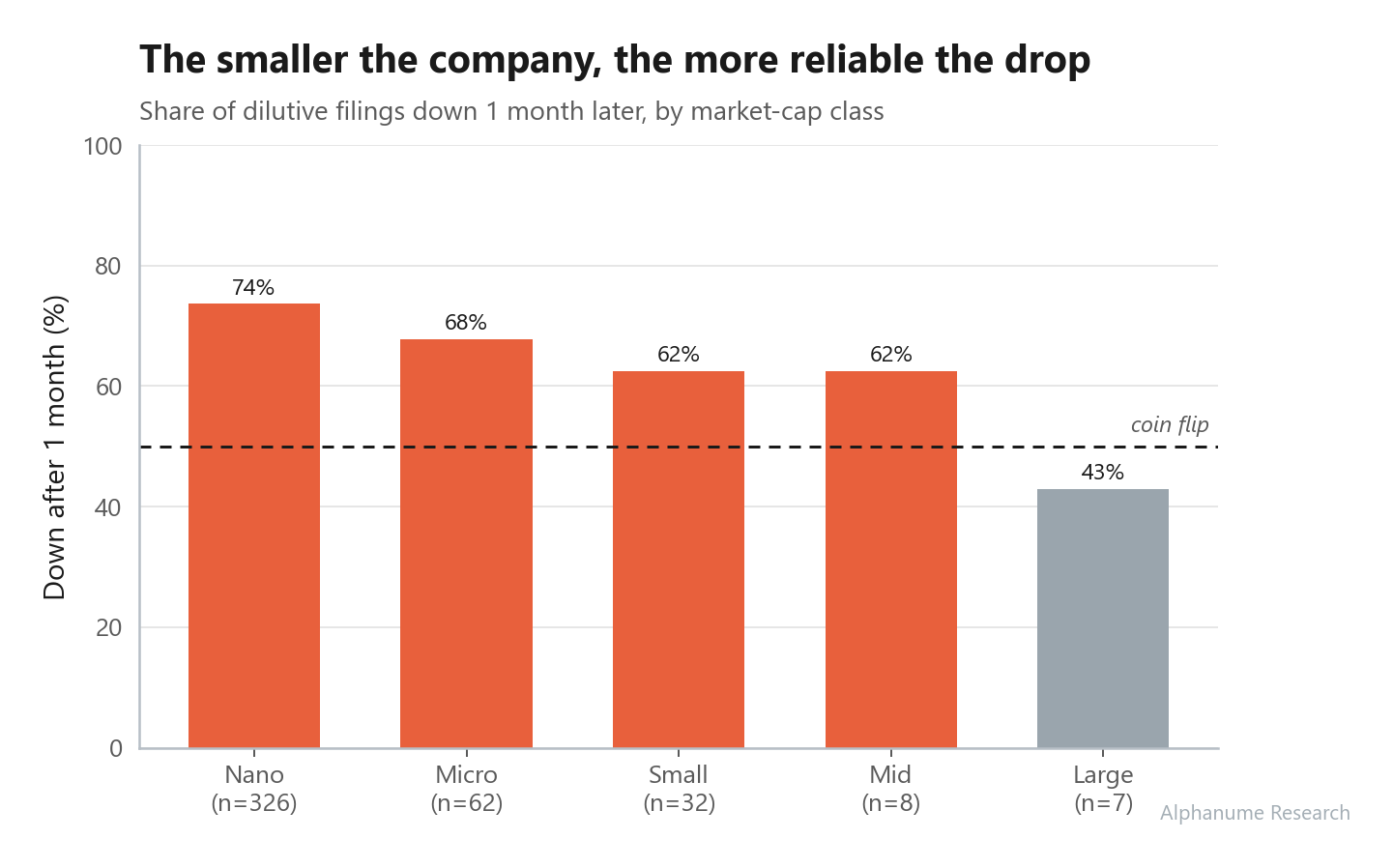

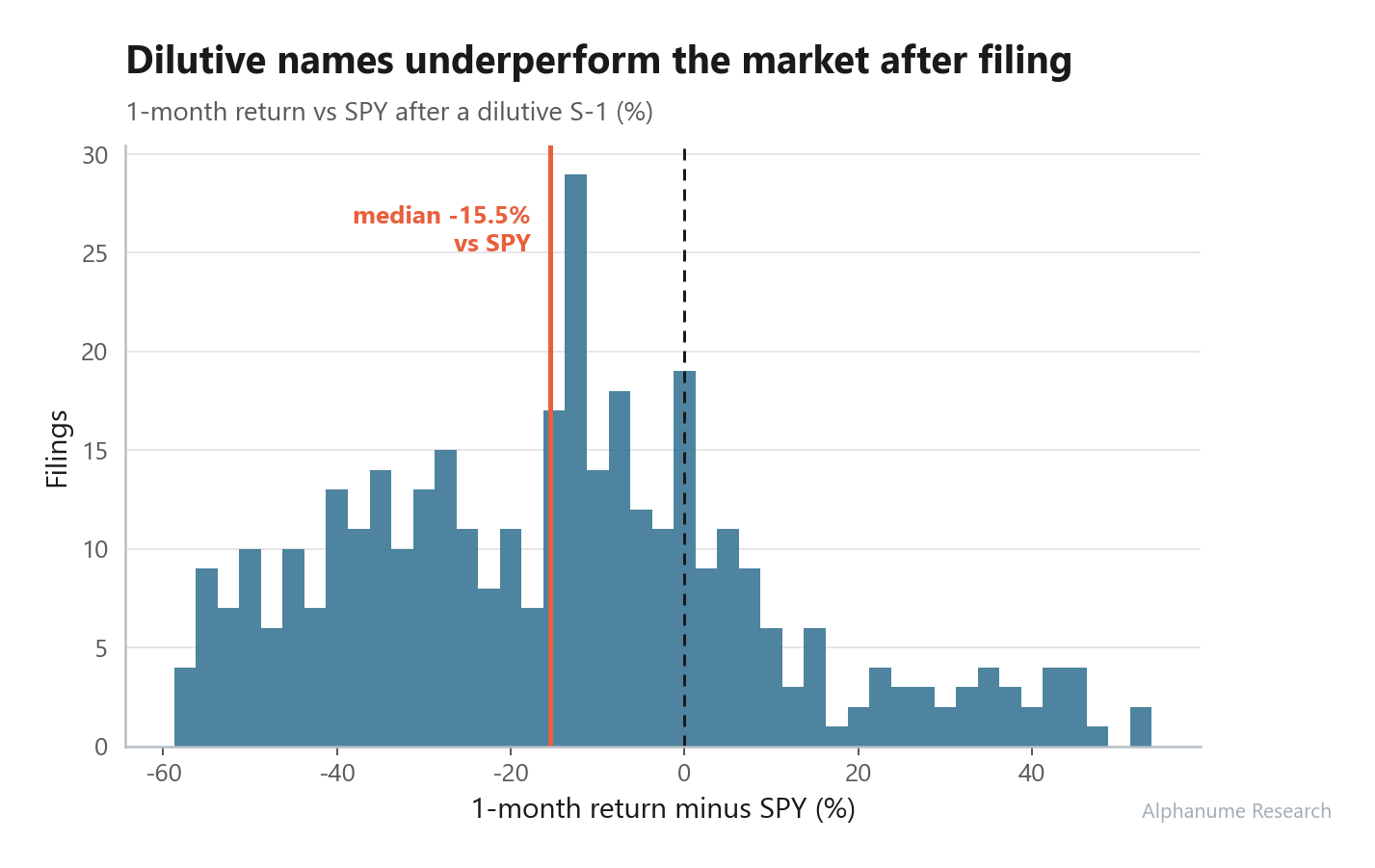

Stock Dilution

Median -14.9% at 1 month (-15.5% vs. SPY), 71% of filings lower (z = 8.9). Monotonic in size: nano-caps 74% down, large-caps 43%.

Strong - 02

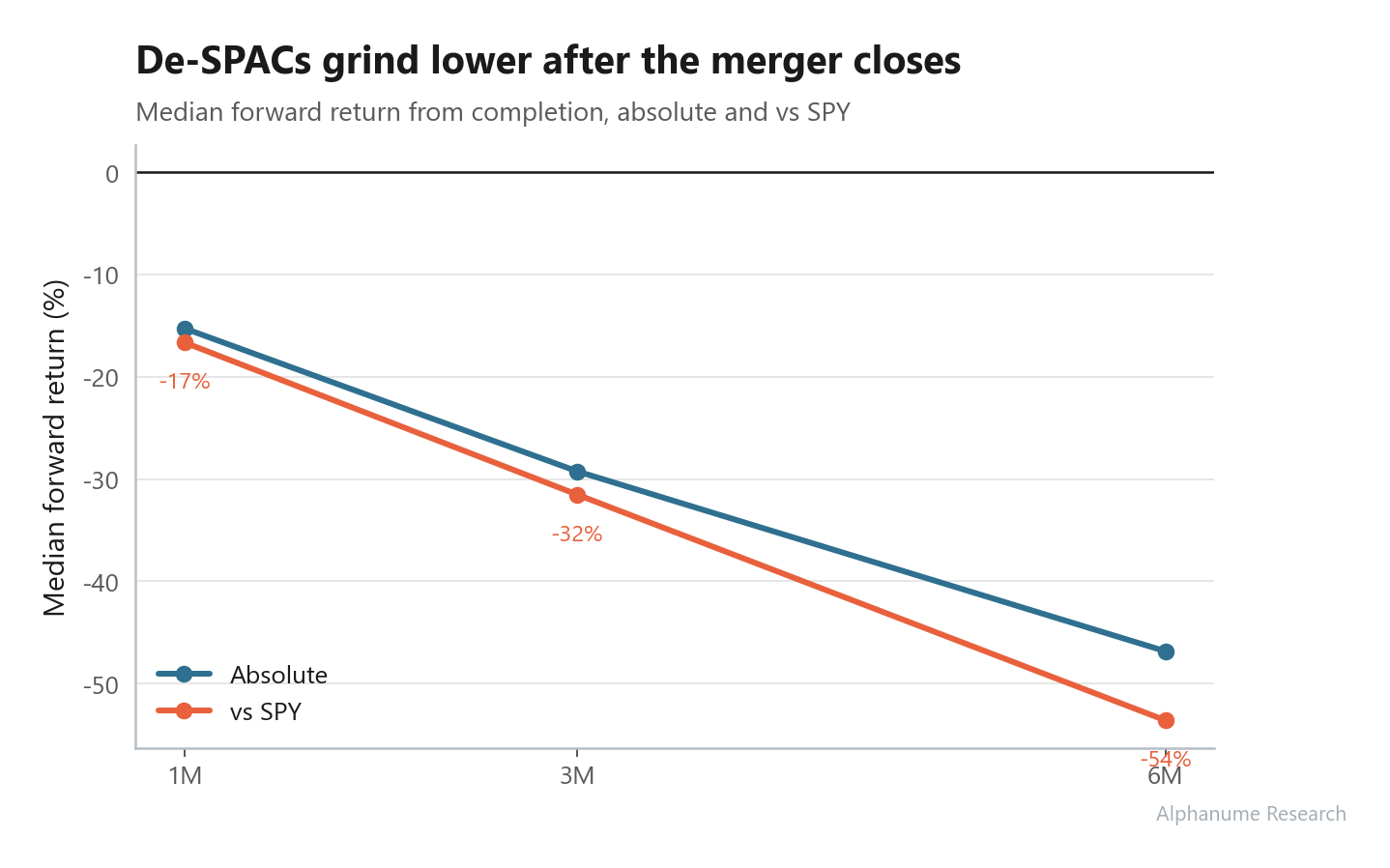

De-SPAC Events

Median -29% at 3 months, -47% at 6 months; 74% lower at 3M (z = 9.3). Heavy redemptions roughly triple the damage (-43% vs. -16%).

Strong - 03

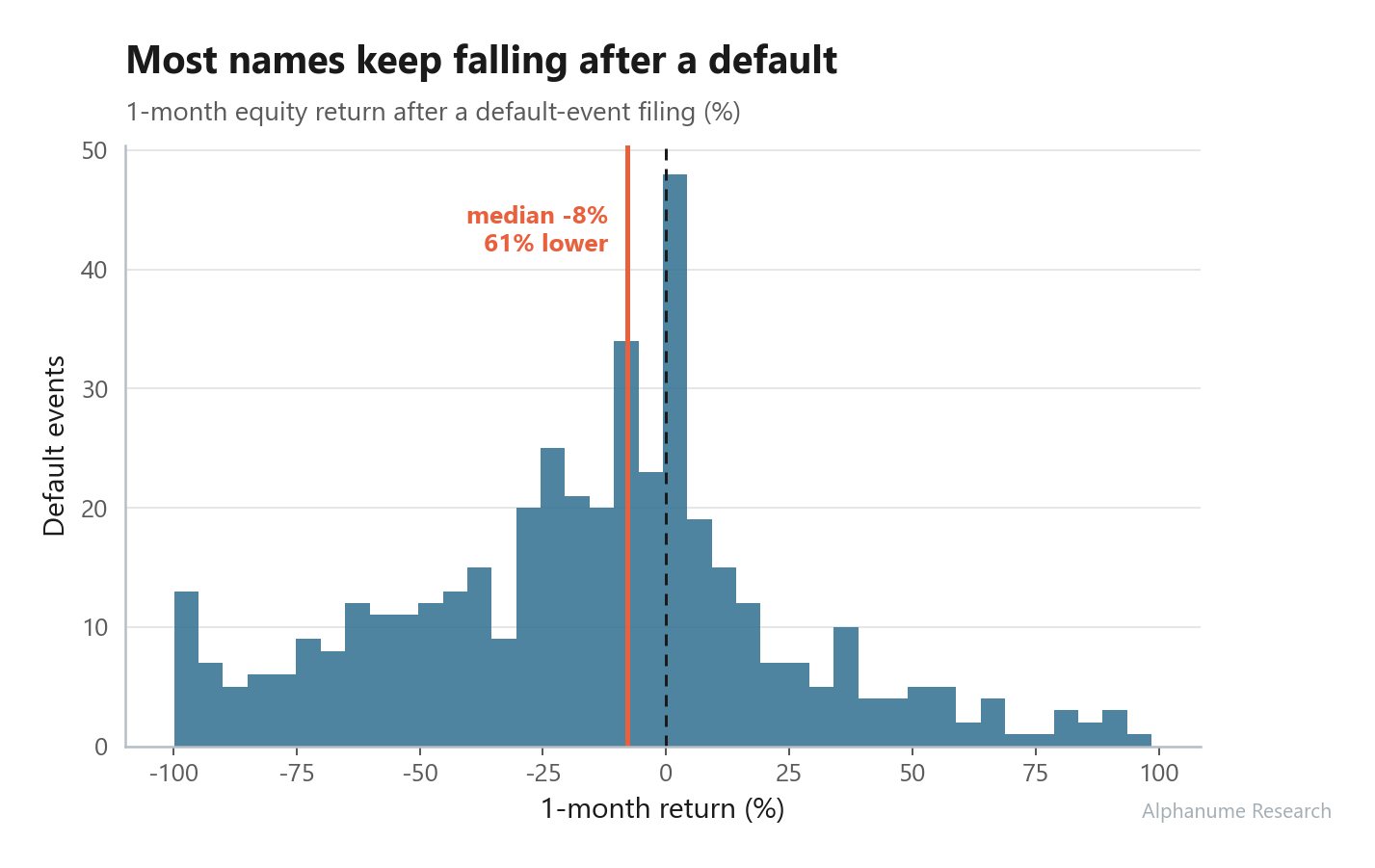

Corporate Default Events

Median -34% at 3 months; 61% lower a month later (z = 4.6). Severity-ordered: missed payments -37%, soft events near flat.

Strong - 04

Earnings Implied vs Realized

Straddles overprice the realized move 64% of the time (z = 16.3), +1.1% of spot per event (t = 10.4); +4,024 points captured cumulatively.

Strong - 05

Next-Day Movers

Selected names realize a 4.8% median move vs. 2.4% on a normal day (2.0x); 5%+ moves hit 48% vs. 24%.

Strong - 06

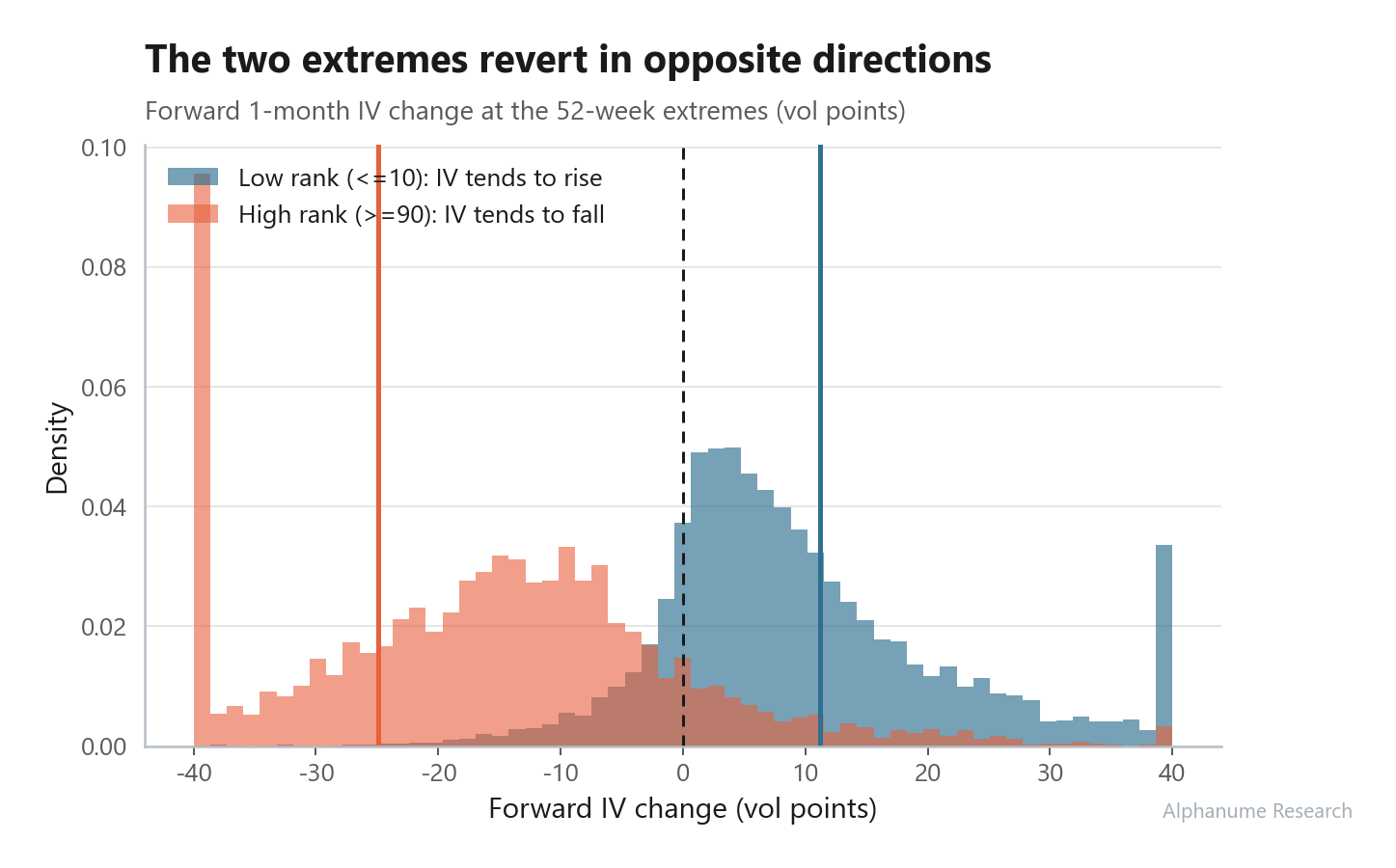

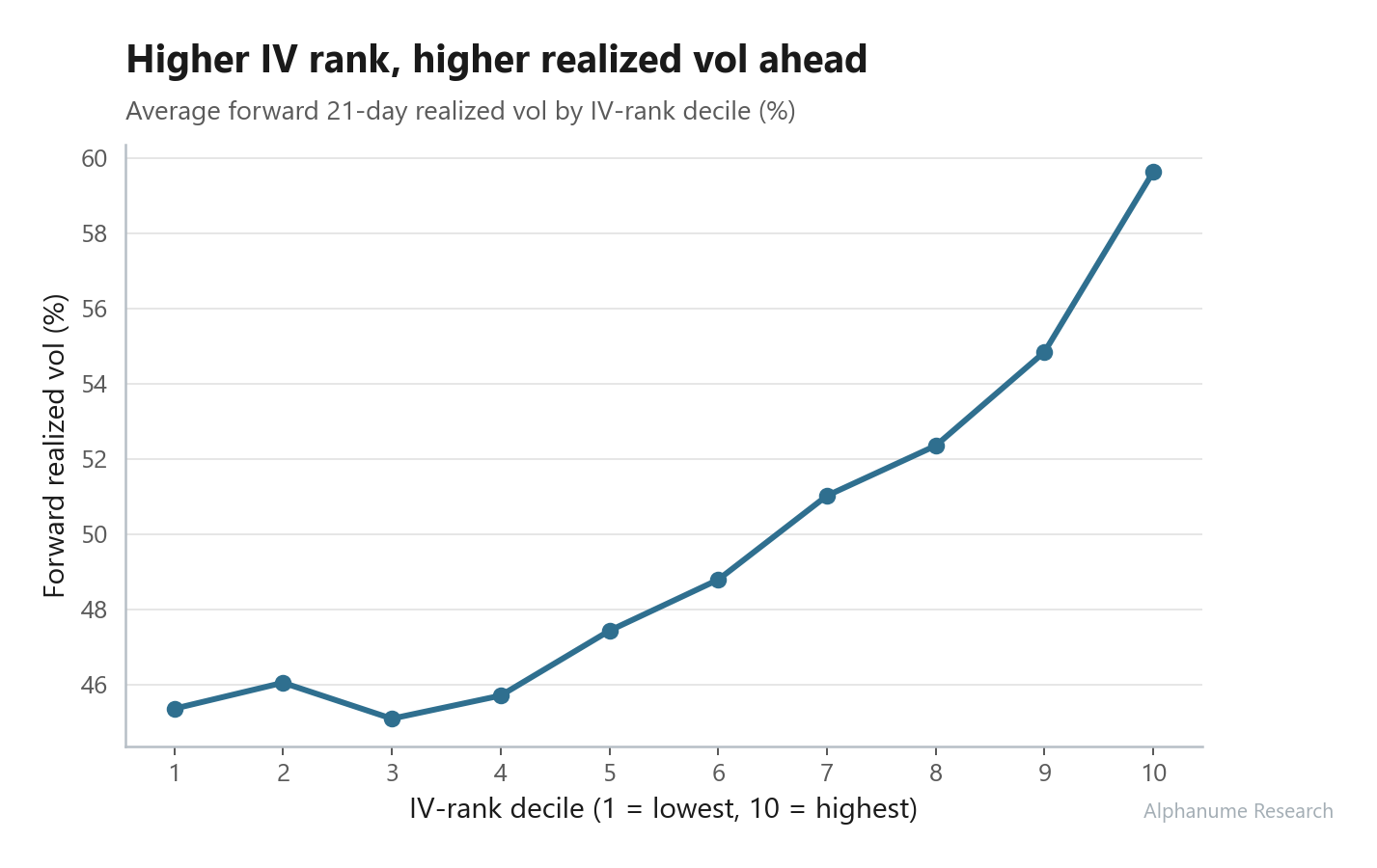

IV/HV Rank (52-Week)

Top-of-range IV falls -24.9 vol points over the next month; bottom rises +11.2. Monotonic across deciles (corr -0.36 on 141k obs).

Strong - 07

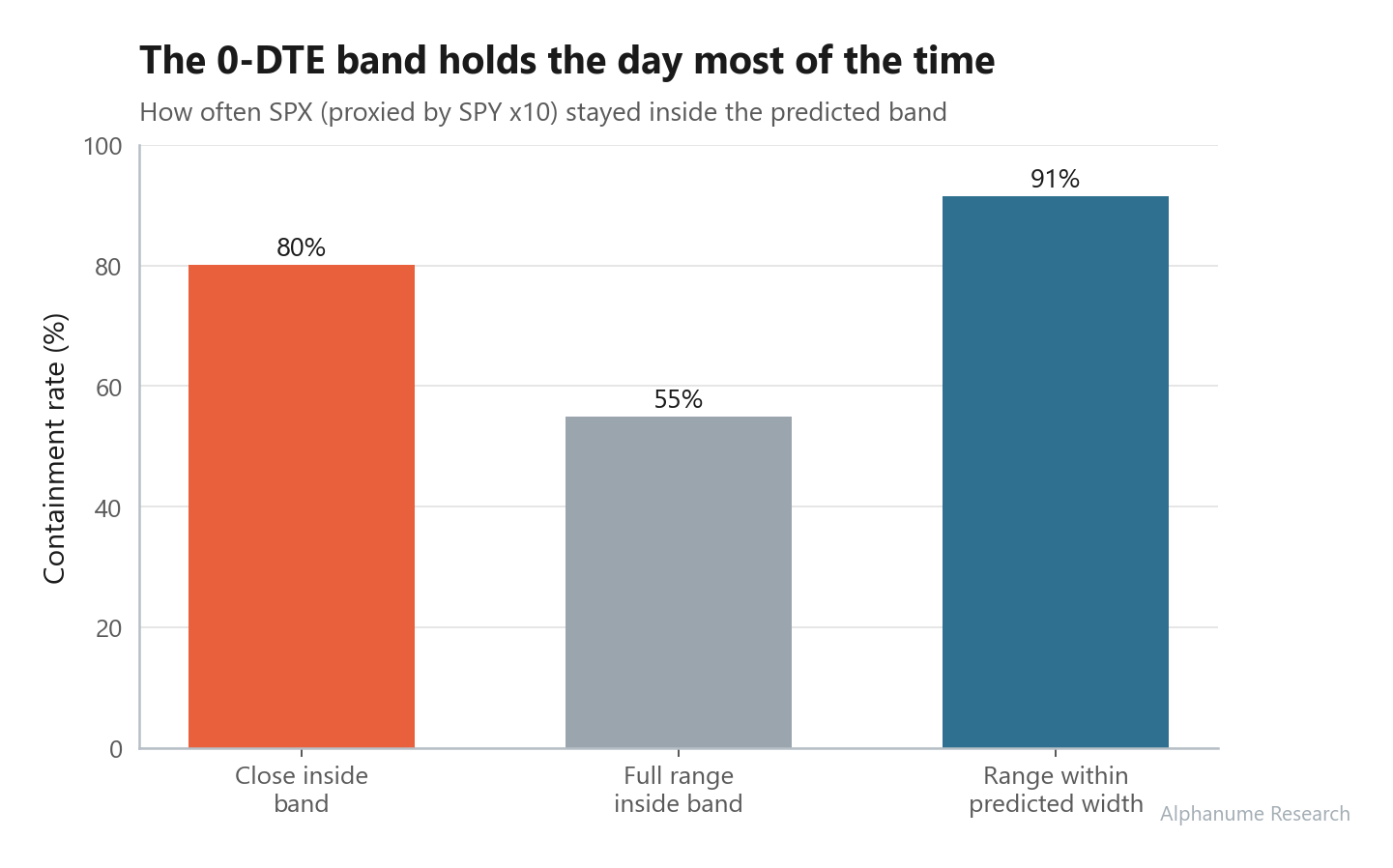

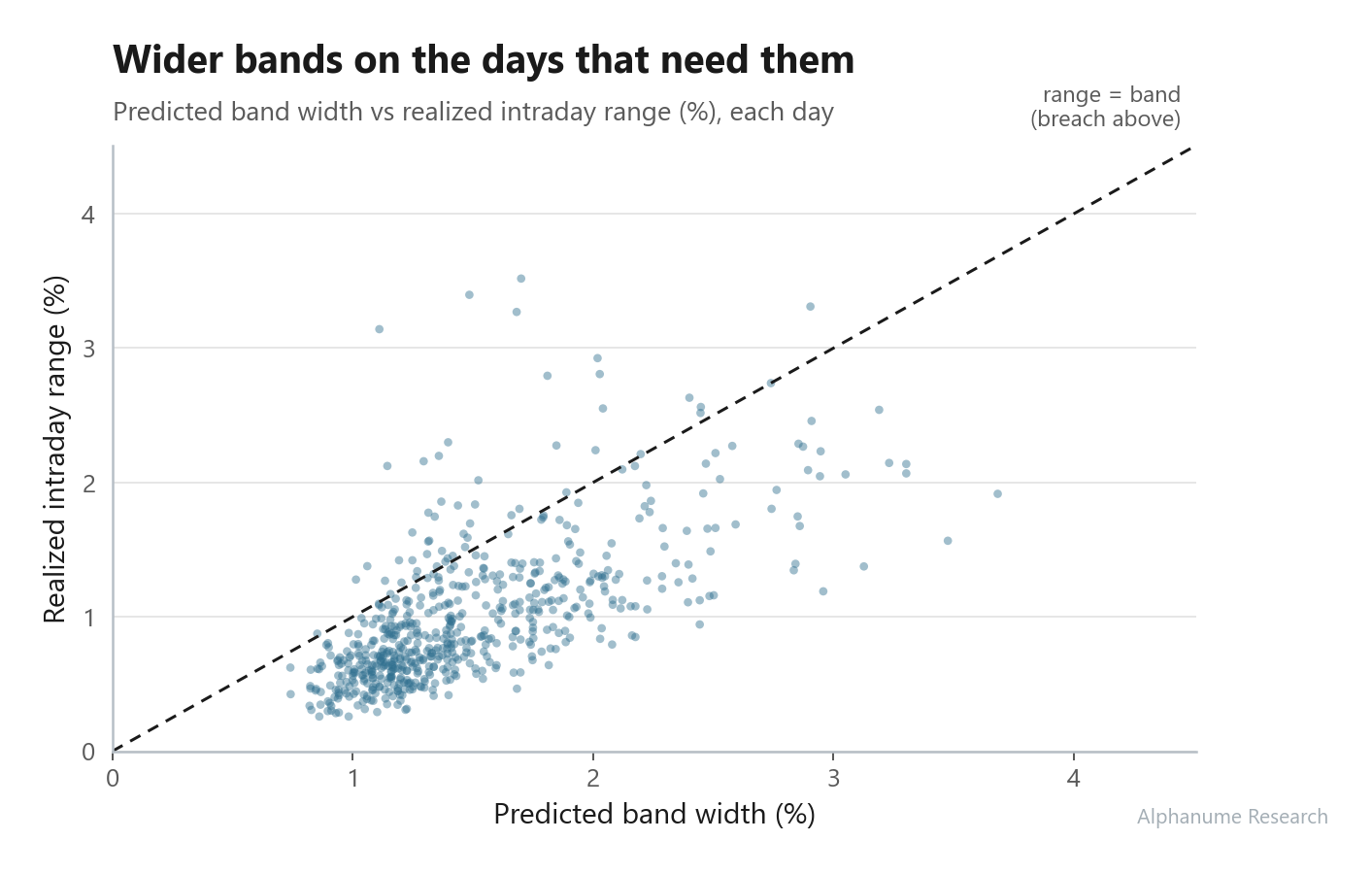

S&P 500 0-DTE Strike Band

Predicted width contains the day 91.5% of the time; 80% close containment; band width correlates 0.80 with the realized range.

Strong - 08

Quant Galore Momentum Index

$1 grows to $30.4 vs. $2.9 for SPY since 2017; beats the benchmark 61% of months, +2.84% mean monthly excess (t = 2.7).

Strong - 09

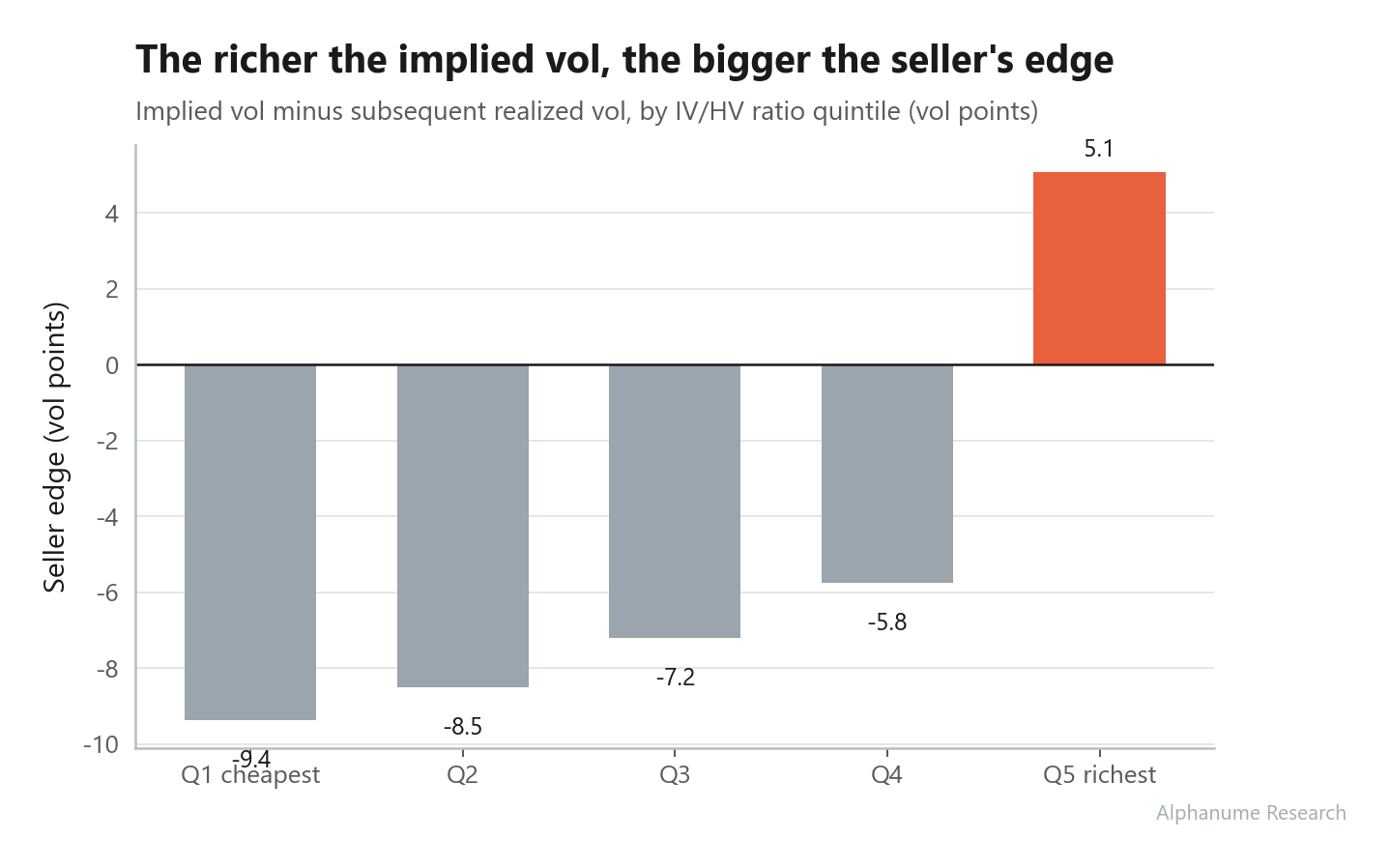

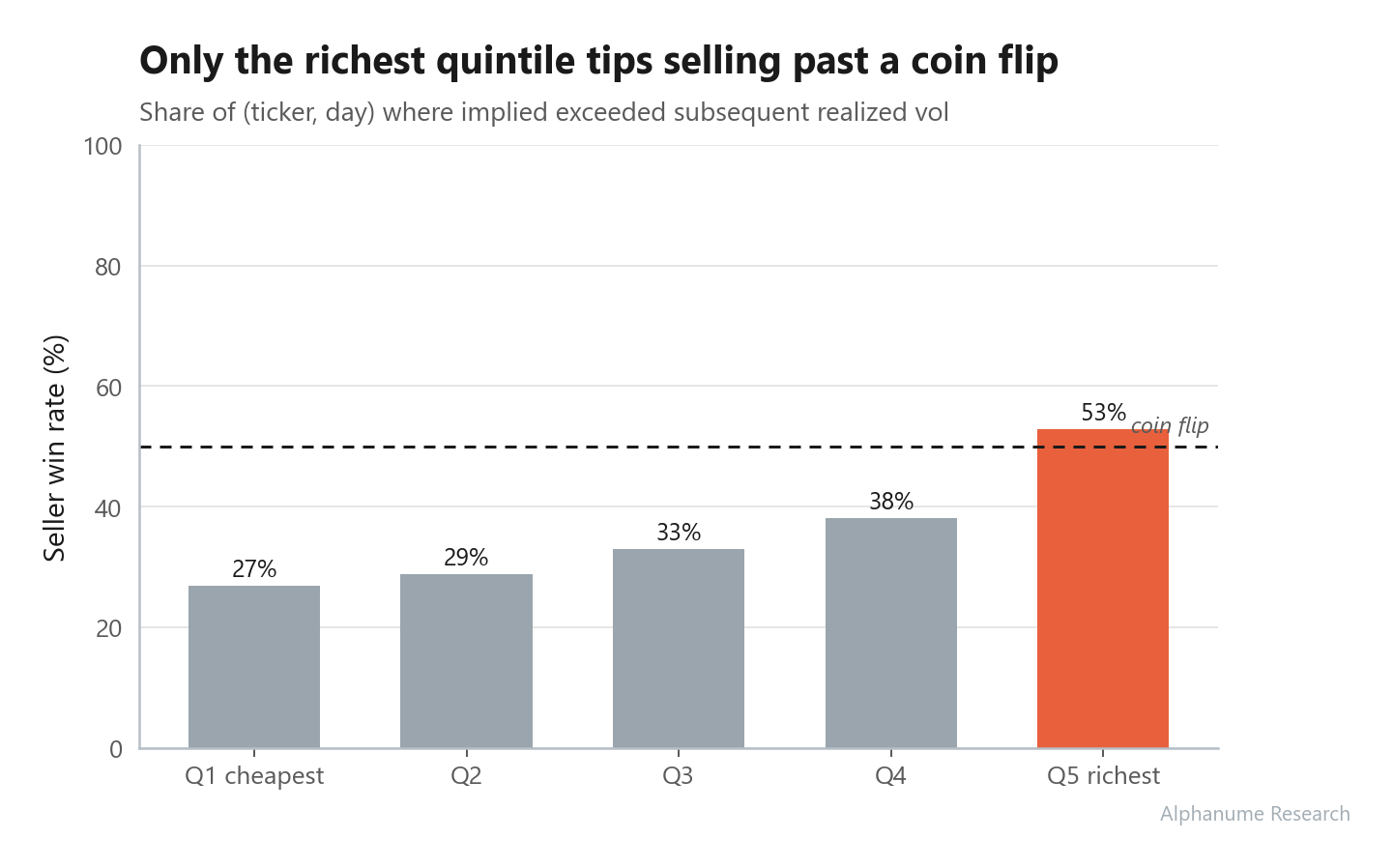

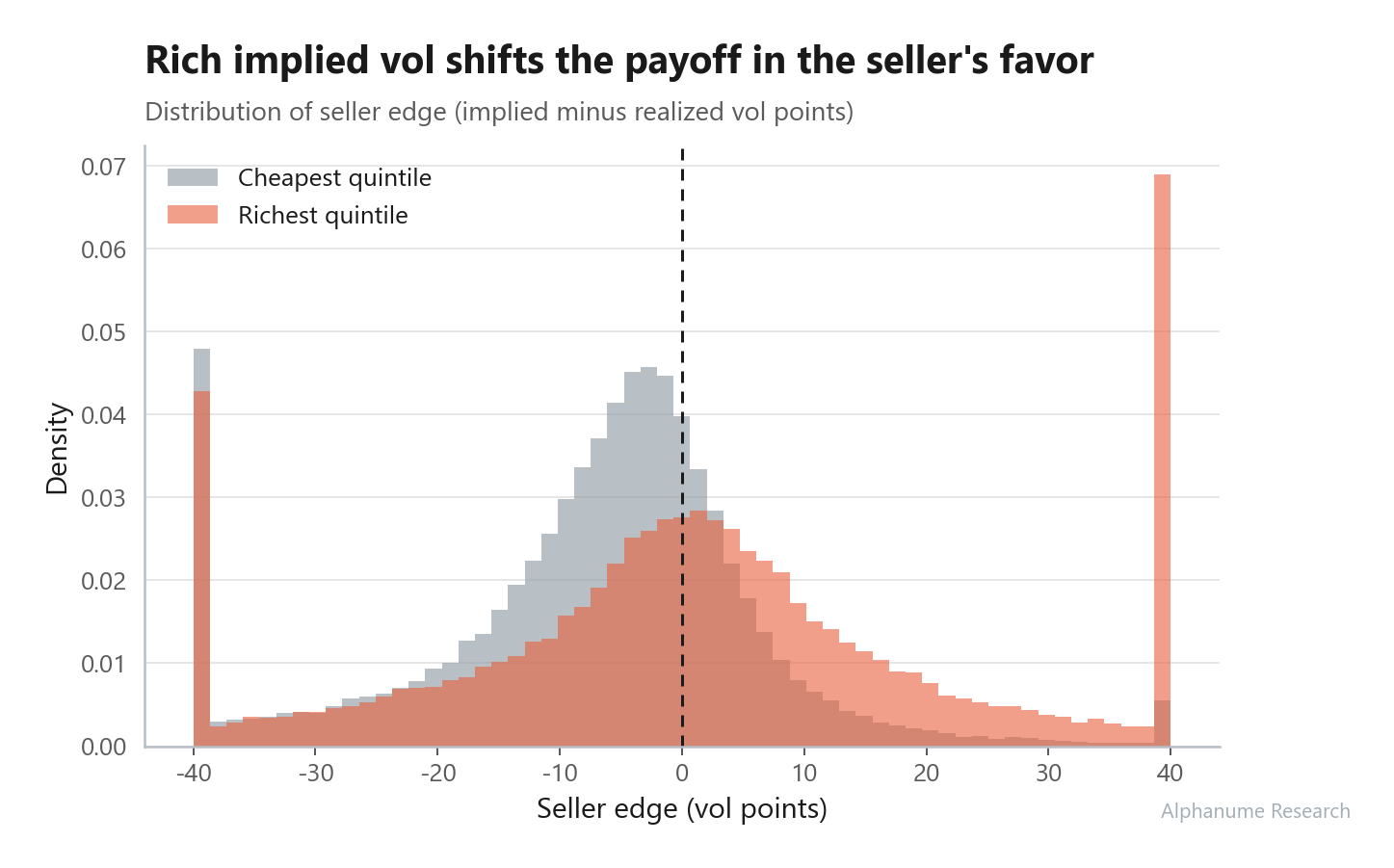

IV/HV Premium

Seller edge sorts monotonically -9.4 to +5.1 vol points across IV/HV-ratio quintiles (14.5-pt long-short spread); win rate 27% to 53%.

Strong - 10

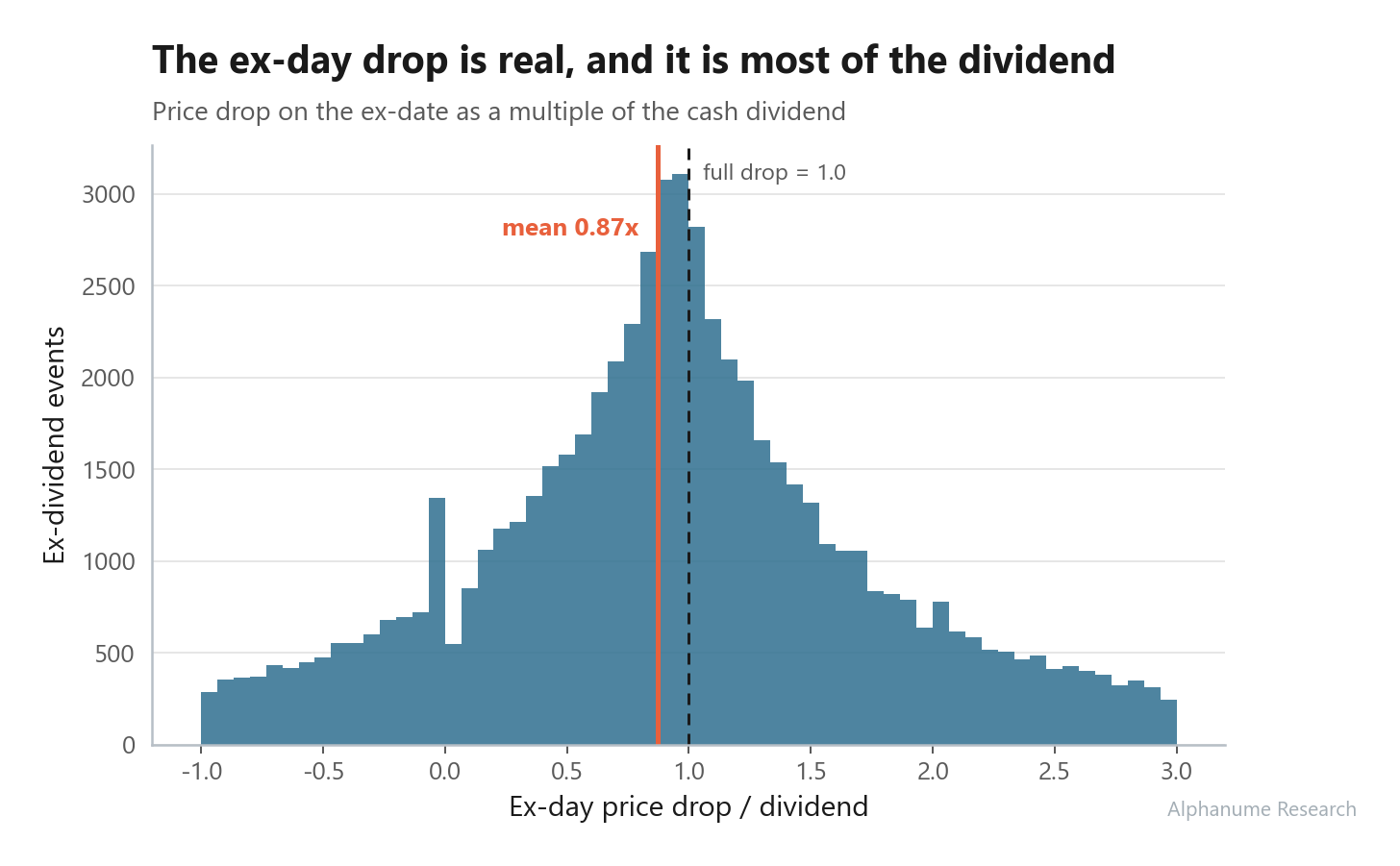

Dividend Capture

Ex-day drop averages 0.87x the dividend; net capture is +0.04% with 45% of events underwater; recovery 55% (1d) to 91% (20d).

Strong - 11

S&P 500 Risk Regime

Risk-off days realize 24.7% vol vs. 12.8% (2x); forward 10-day vol 19.0% vs. 12.3% (t = 15.0). Returns: 13.0% vs. 12.7%, not directional.

Nuanced - 12

Vol-of-Vol Index

Correlation with forward vol is just 0.05 and non-monotonic. At the extreme it works: the top decile realizes 61% vol and 11% max moves vs. ~8% elsewhere.

Nuanced

The rigor, stated plainly, including where the proxy is rough.

- 01

Tested against real prices

Signals come from the Alphanume API; outcomes are measured against adjusted daily bars from Polygon. Samples run from a few hundred events to north of 290,000 name-days, depending on the dataset.

- 02

Benchmarked and significance-tested

Excess returns are taken versus SPY wherever a market comparison is meaningful. Every result carries a real test (a win-rate z-stat, a t-stat, monotonic bucketing, or a long-short spread), not just a median.

- 03

Point-in-time by construction

Each observation is stamped as it became available, not as it looks in hindsight. No survivorship, no silent revisions, no lookahead leaking into the study.

- 04

Gross, and honest about it

Premium-capture figures are gross of transaction costs, slippage, and path/gamma; they establish an edge's existence and stability, not a net Sharpe. The weak links (vol-of-vol, the SPY x10 SPX proxy, conditional vol-selling) are stated next to the numbers, not hidden.

Stock Dilution

437 dilutive S-1 filings + 328 controls · Jan 2025–presentA point-in-time record of S-1 registration statements, flagged dilutive vs. non-dilutive. The dilutive flag is a supply-shock signal, most violent in the smallest caps, where a secondary offering is enormous relative to float.

Median -14.9% at 1 month (-15.5% vs. SPY), 71% of filings lower (z = 8.9). Monotonic in size: nano-caps 74% down, large-caps 43%.

01.1Dilutive vs. non-dilutive forward returns

01.2Short success rate by market-cap class

01.31-month SPY-excess return distribution

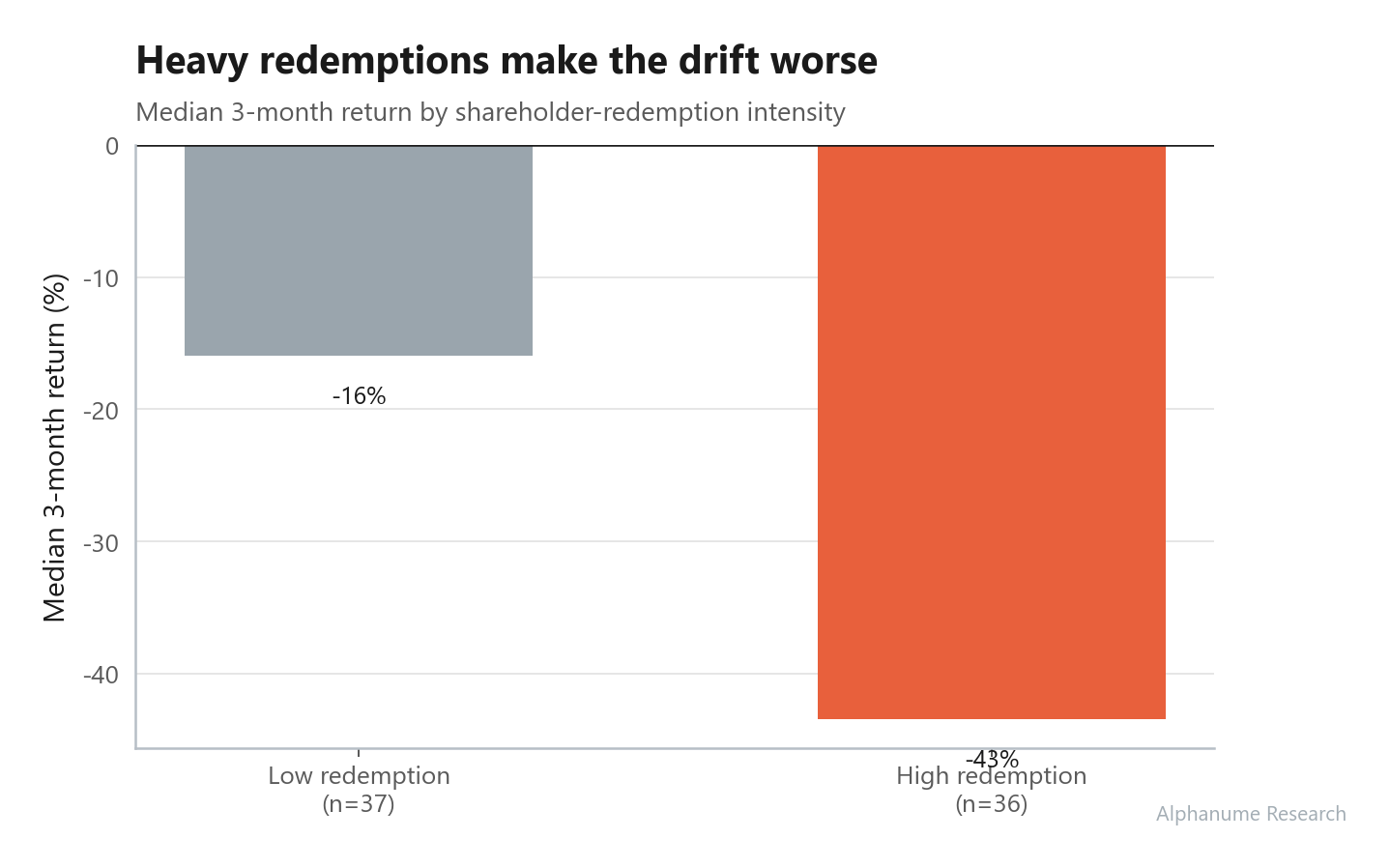

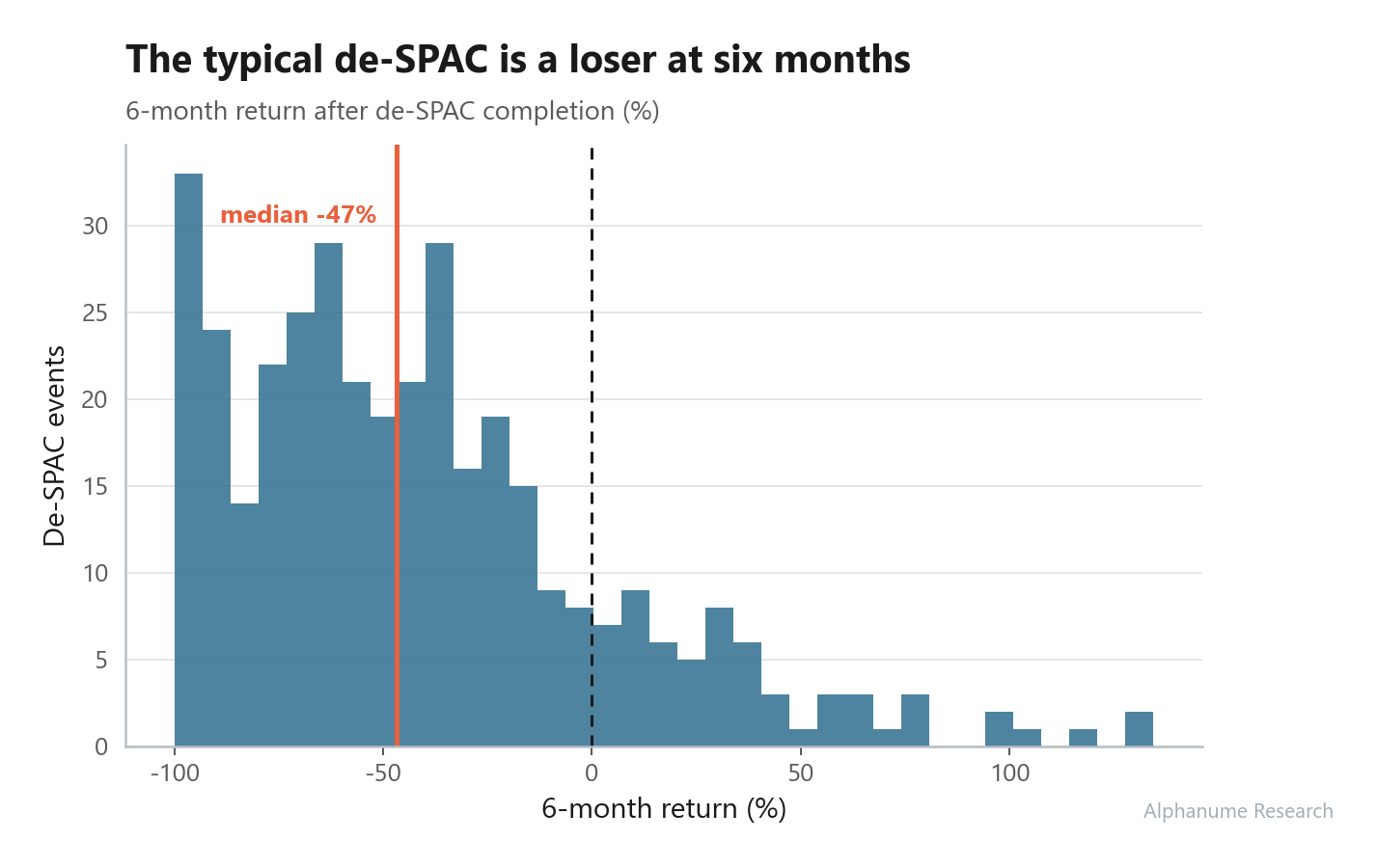

De-SPAC Events

371 completed de-SPACs · 2020–presentCompleted SPAC-to-operating-company mergers, parsed from SEC filings. A structurally challenged cohort that tends to drift down after completion, and harder when shareholders redeem heavily.

Median -29% at 3 months, -47% at 6 months; 74% lower at 3M (z = 9.3). Heavy redemptions roughly triple the damage (-43% vs. -16%).

02.1Median forward drift, absolute and vs. SPY

02.23-month return by redemption intensity

02.36-month return distribution

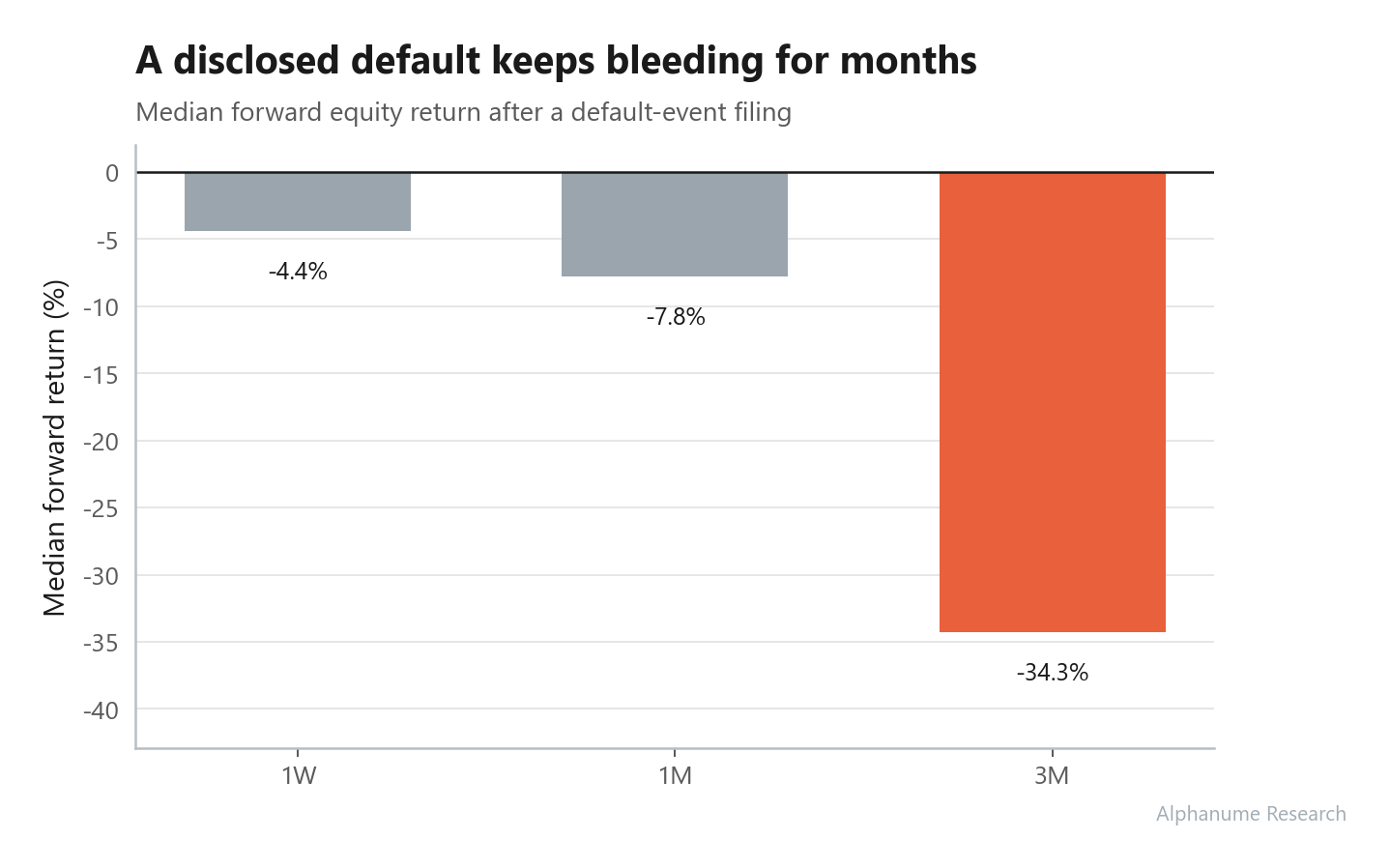

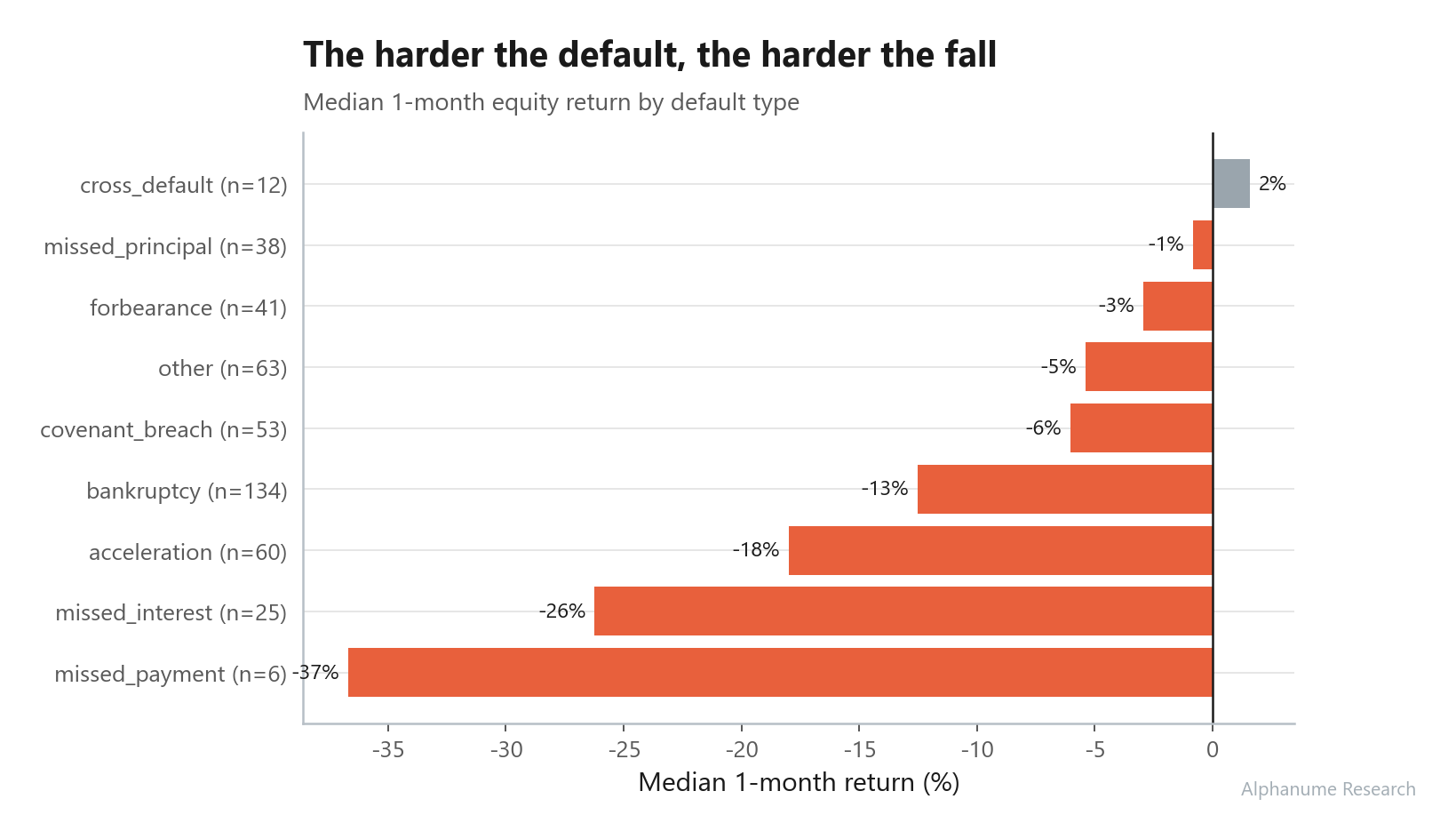

Corporate Default Events

472 default events · 2020–presentPublic-company default events labeled from SEC filing text: missed payments, covenant breaches, accelerations, bankruptcies. A hard credit signal that keeps hurting the equity after disclosure.

Median -34% at 3 months; 61% lower a month later (z = 4.6). Severity-ordered: missed payments -37%, soft events near flat.

03.1Median forward return after default

03.2Median 1-month return by default type

03.31-month return distribution

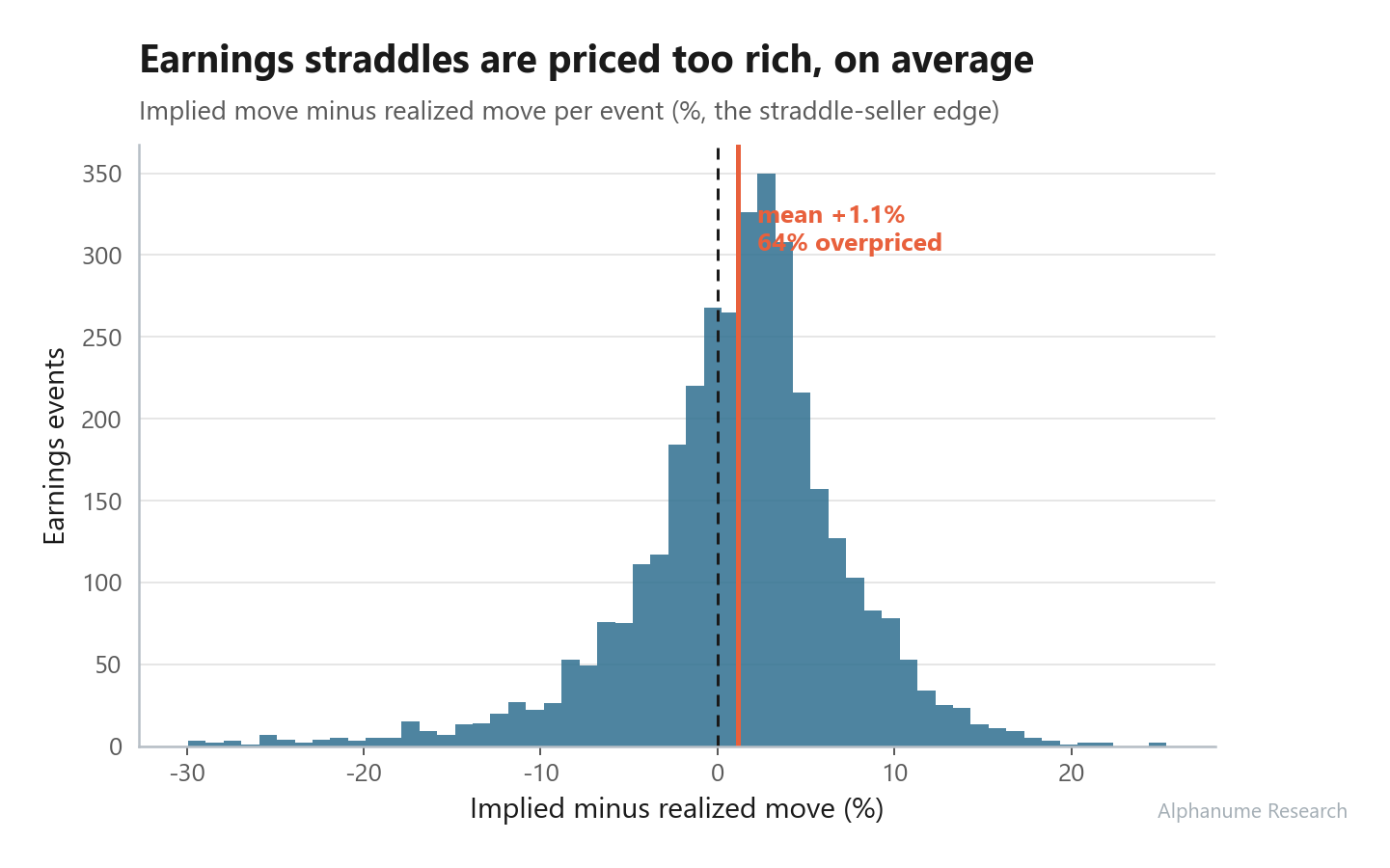

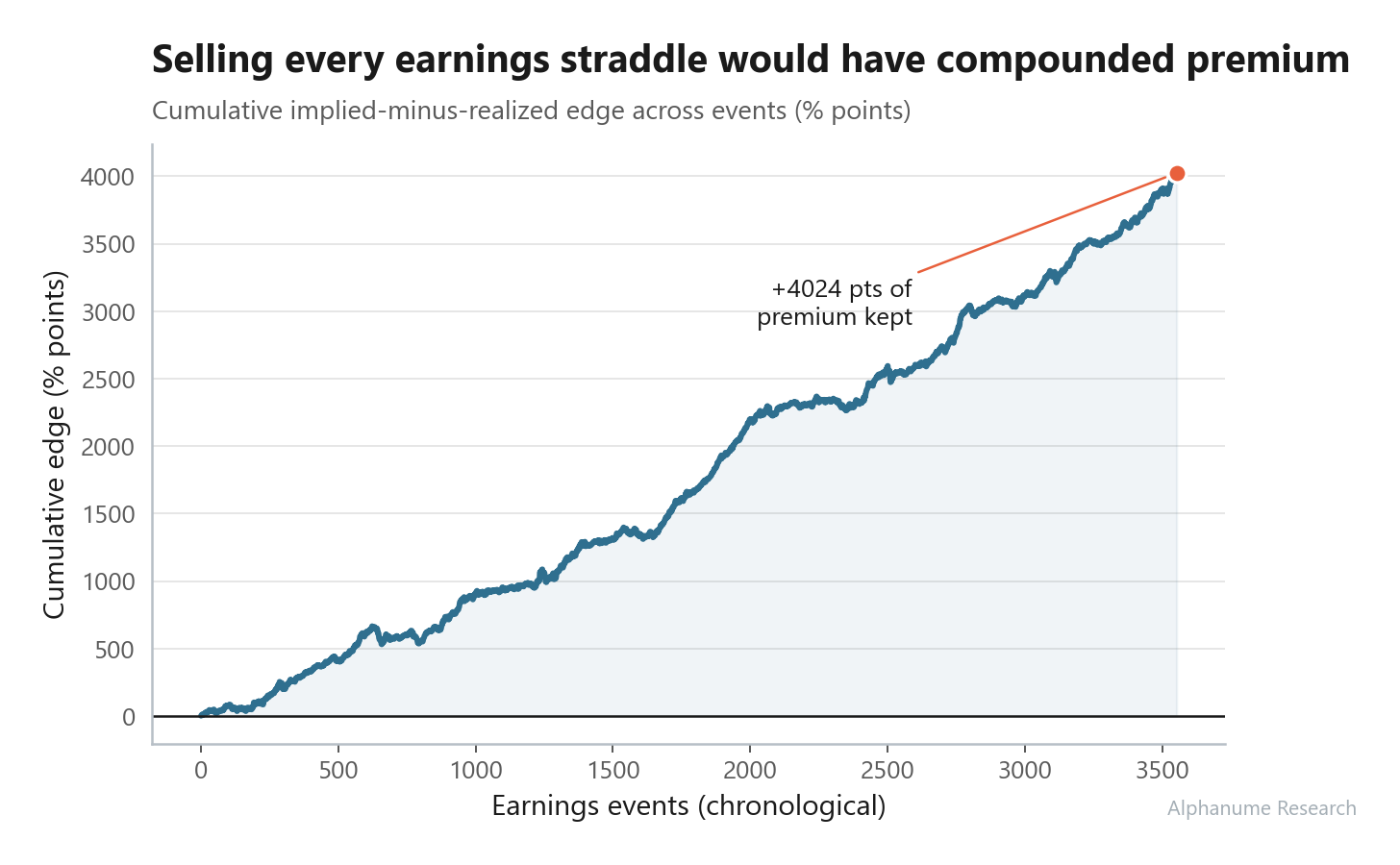

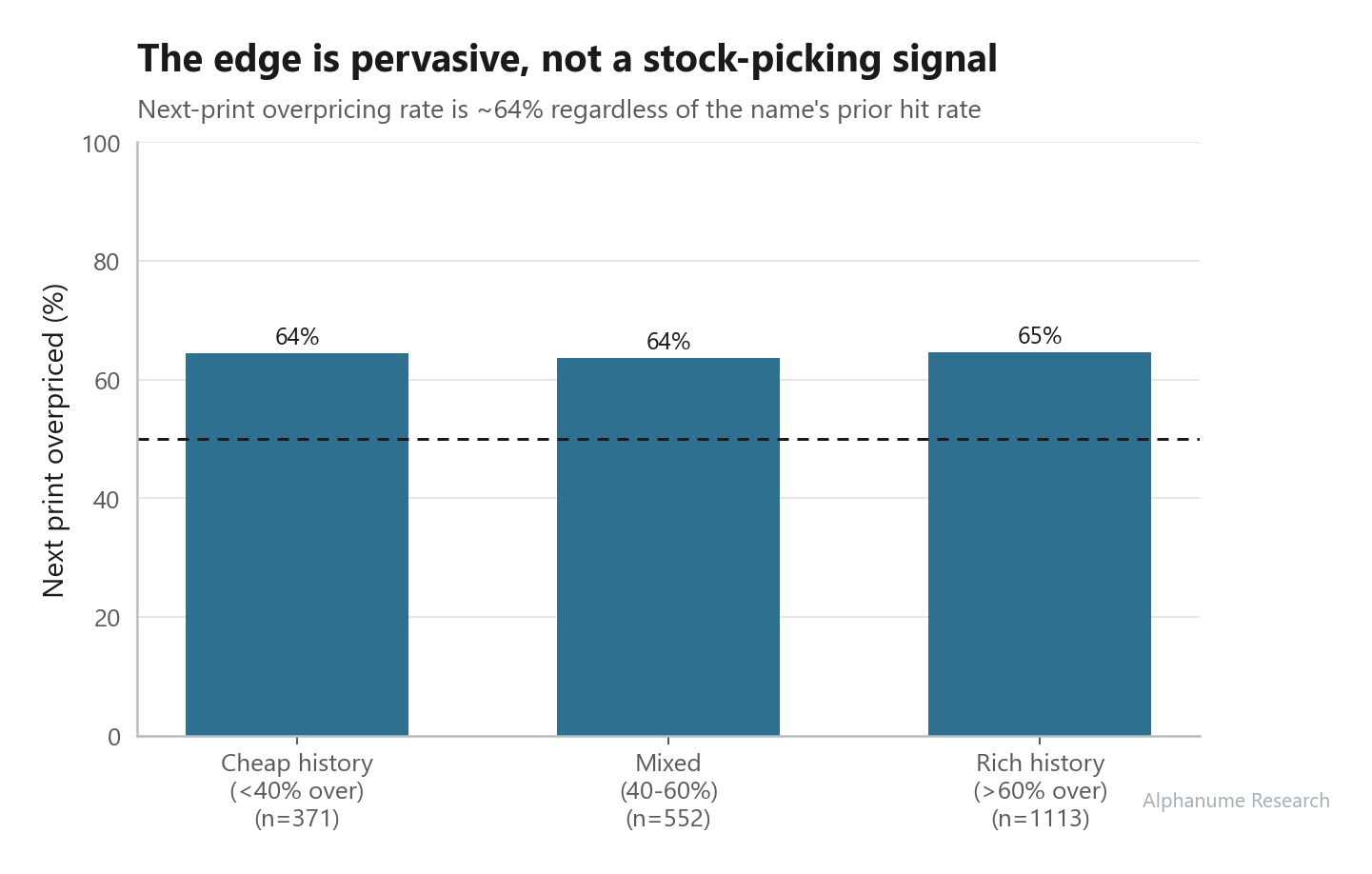

Earnings Implied vs Realized

3,554 earnings events · 2024–presentA per-name track record of how each earnings move was priced (pre-earnings ATM straddle) versus how it actually moved. A direct read on the volatility risk premium. Gross of costs; the premium is market-wide, not name-specific.

Straddles overprice the realized move 64% of the time (z = 16.3), +1.1% of spot per event (t = 10.4); +4,024 points captured cumulatively.

04.1Straddle-seller edge distribution

04.2Cumulative seller edge

04.3Overpricing rate by prior track record

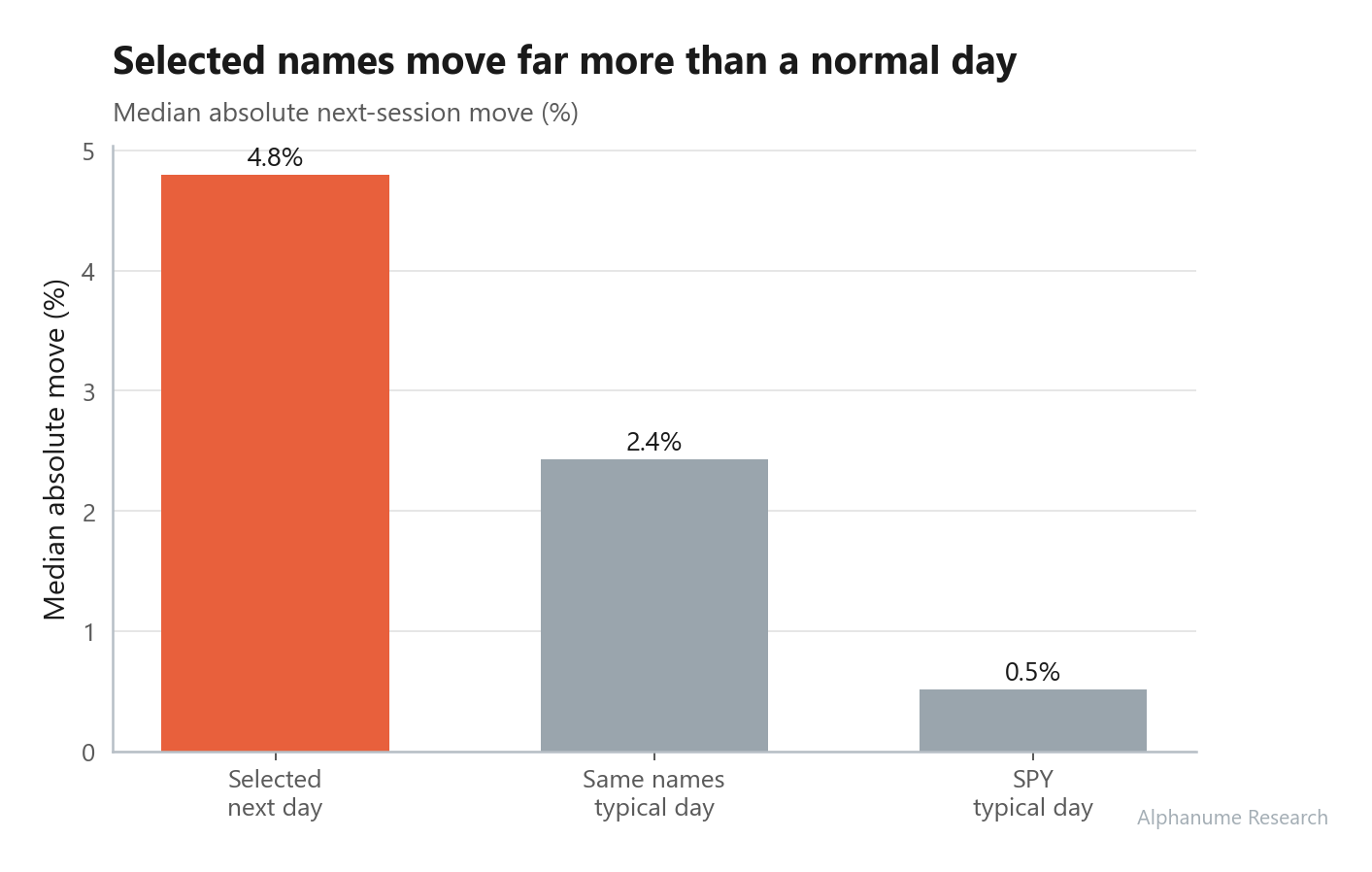

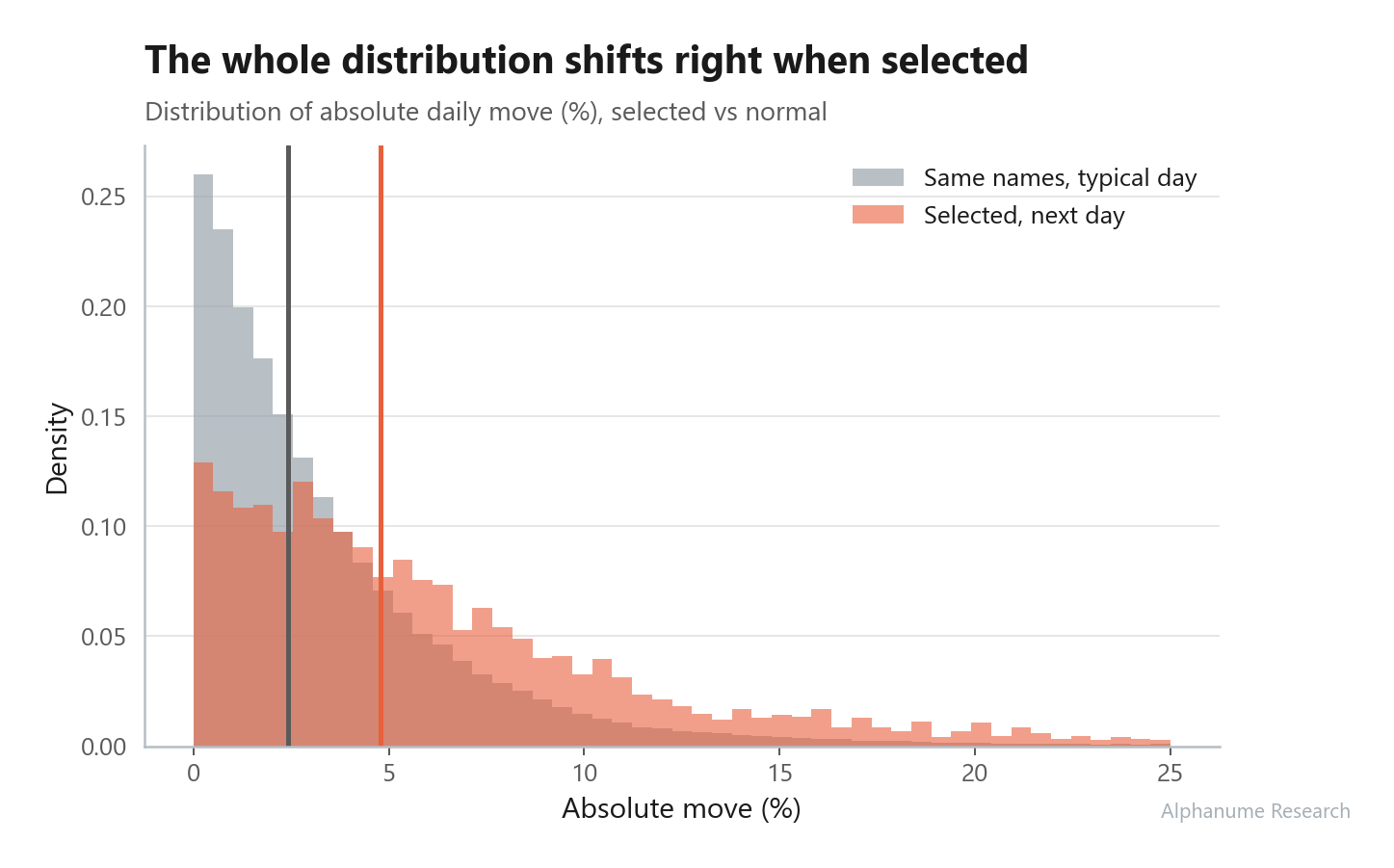

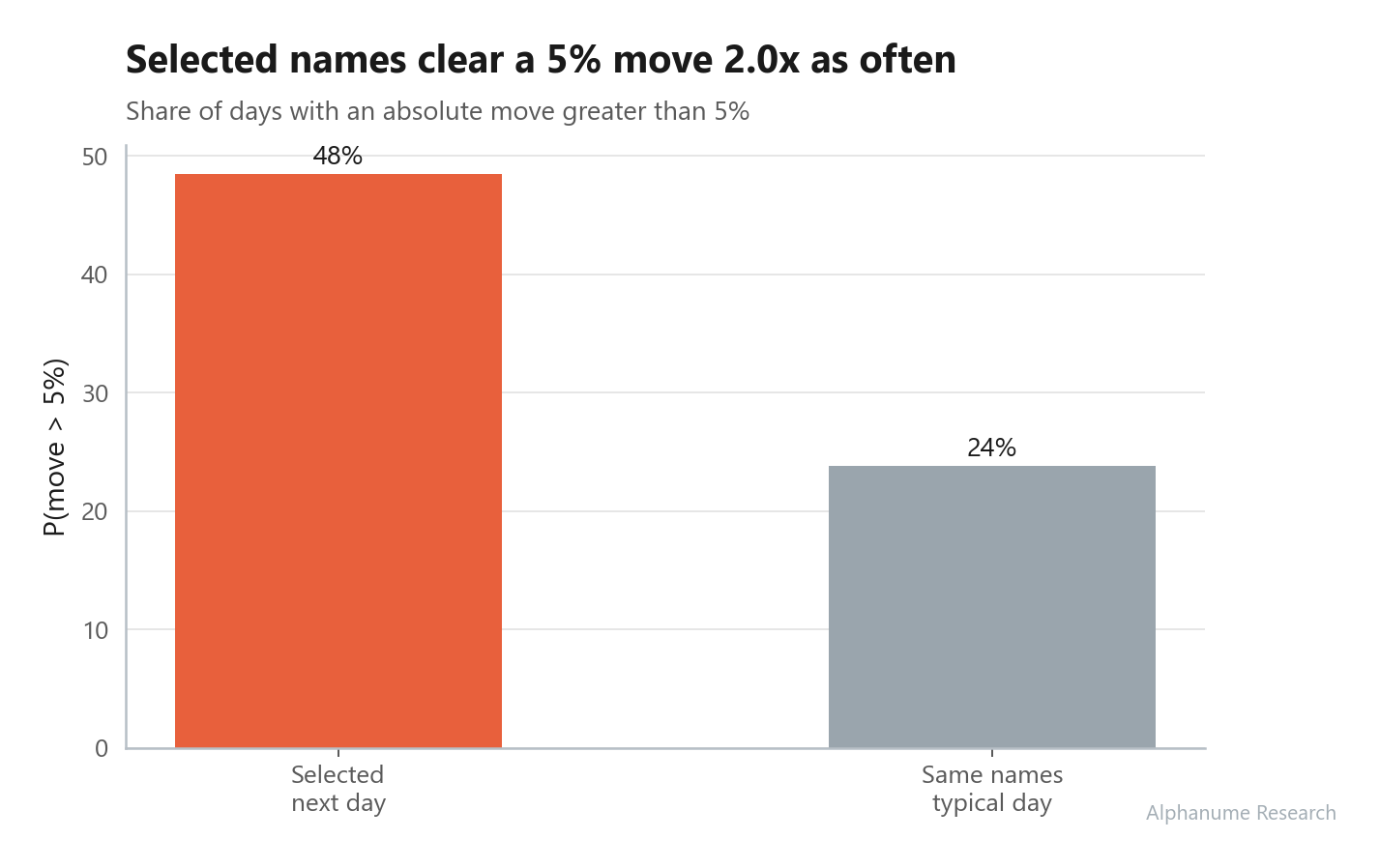

Next-Day Movers

3,005 selections across 157 names · Jan 2024–presentEach afternoon, the equities the model rates most likely to make a large move next session. A magnitude signal (it makes no directional claim), built for non-directional vol trades and movement screens.

Selected names realize a 4.8% median move vs. 2.4% on a normal day (2.0x); 5%+ moves hit 48% vs. 24%.

05.1Median absolute move comparison

05.2Distribution shift, selected vs. normal

05.3Big-move hit rate

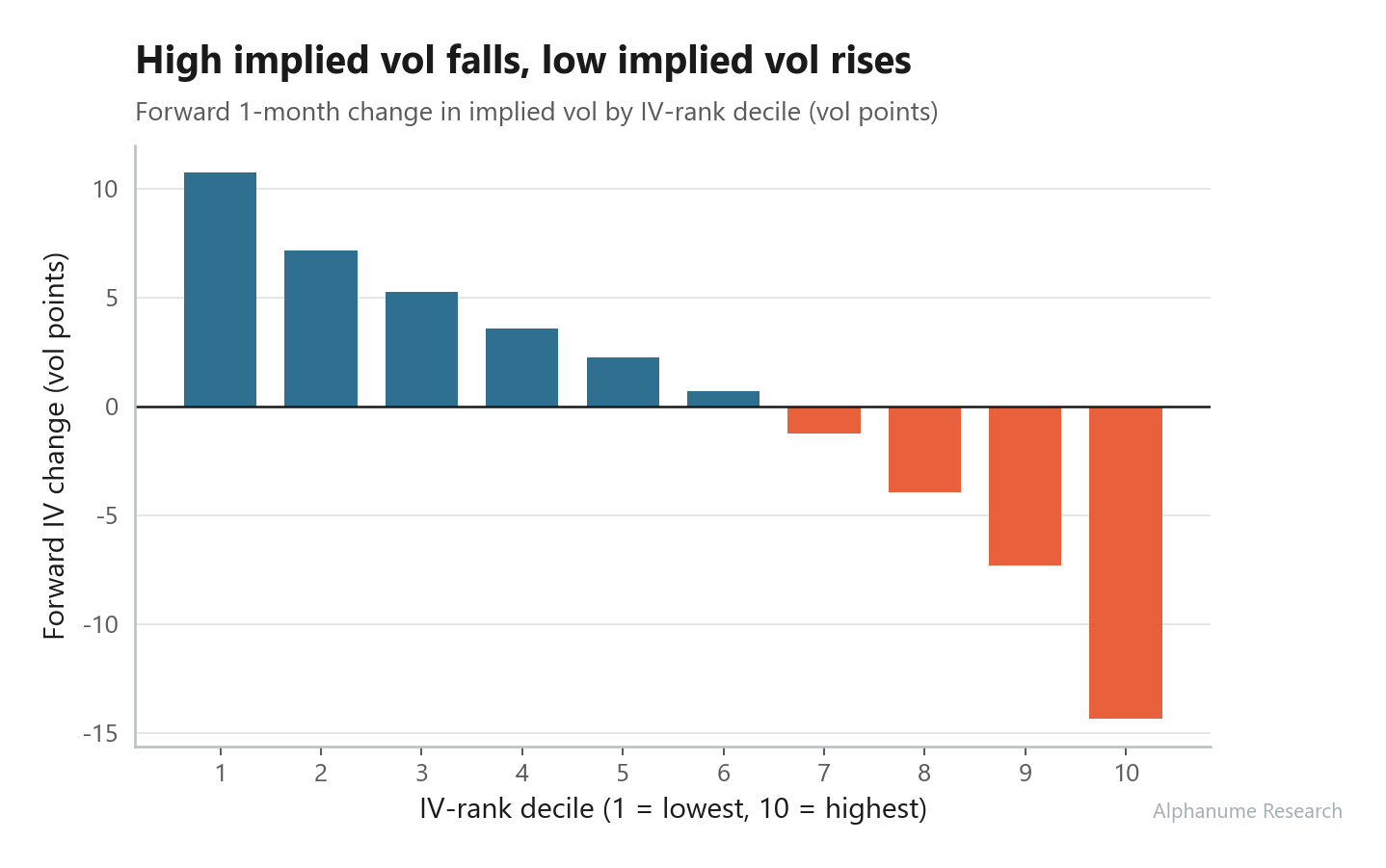

IV/HV Rank (52-Week)

141,169 settled rows · Dec 2024–presentWhere a name's implied and realized vol sit inside their own trailing 52-week range. Extremes mean-revert, which makes the rank a clean timing signal for buying vs. selling premium.

Top-of-range IV falls -24.9 vol points over the next month; bottom rises +11.2. Monotonic across deciles (corr -0.36 on 141k obs).

06.1Forward IV change by IV-rank decile

06.2Reversion at the two extremes

06.3Forward realized vol by decile

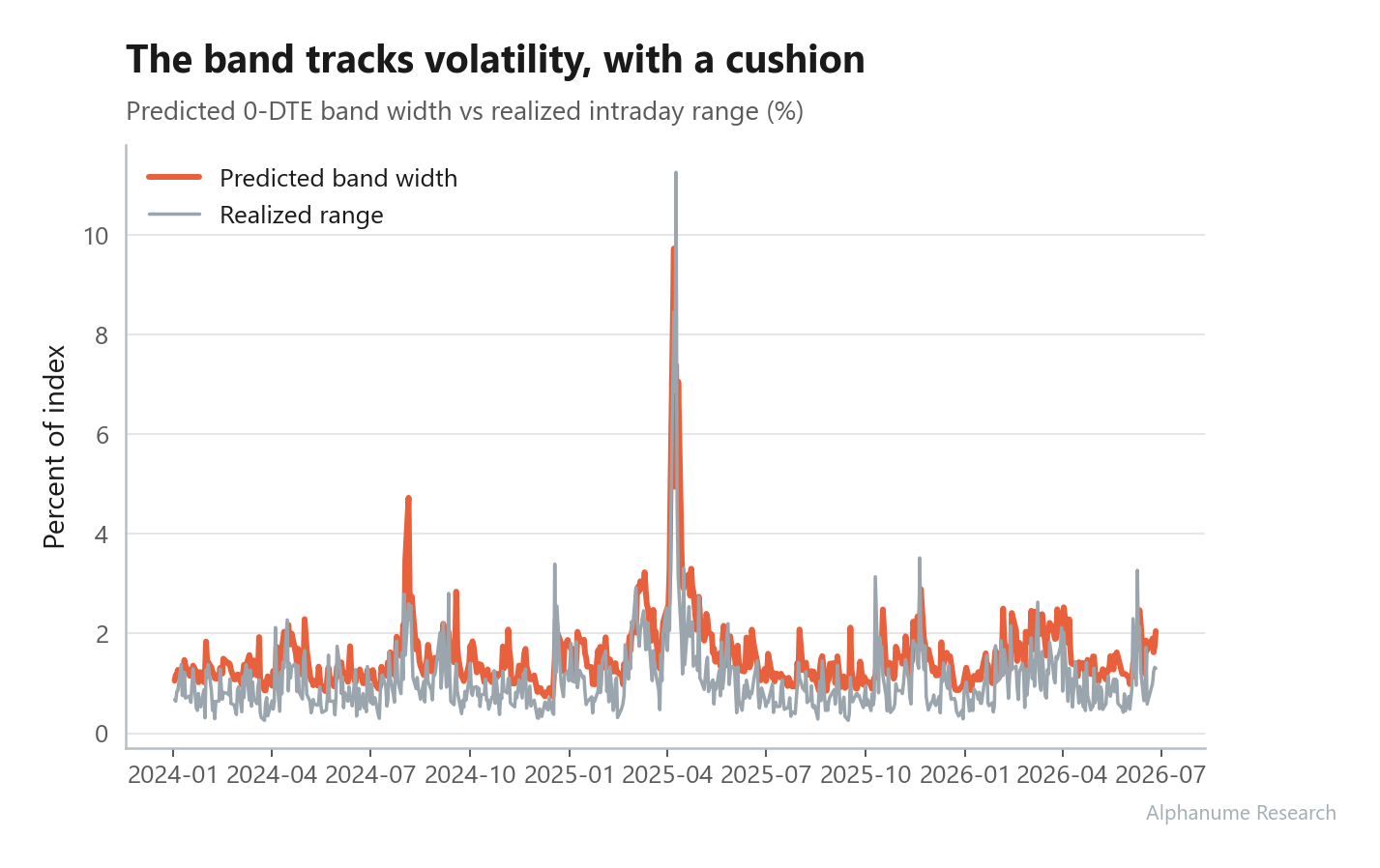

S&P 500 0-DTE Strike Band

622 trading days · Jan 2024–presentThe morning strike range SPX is expected to hold through the same-day 0-DTE close. A calibrated expected-move for strike selection. (SPX is proxied here by SPY x10; tests are run basis-free.)

Predicted width contains the day 91.5% of the time; 80% close containment; band width correlates 0.80 with the realized range.

07.1Containment rates

07.2Predicted width vs. realized range

07.3Band width vs. realized range over time

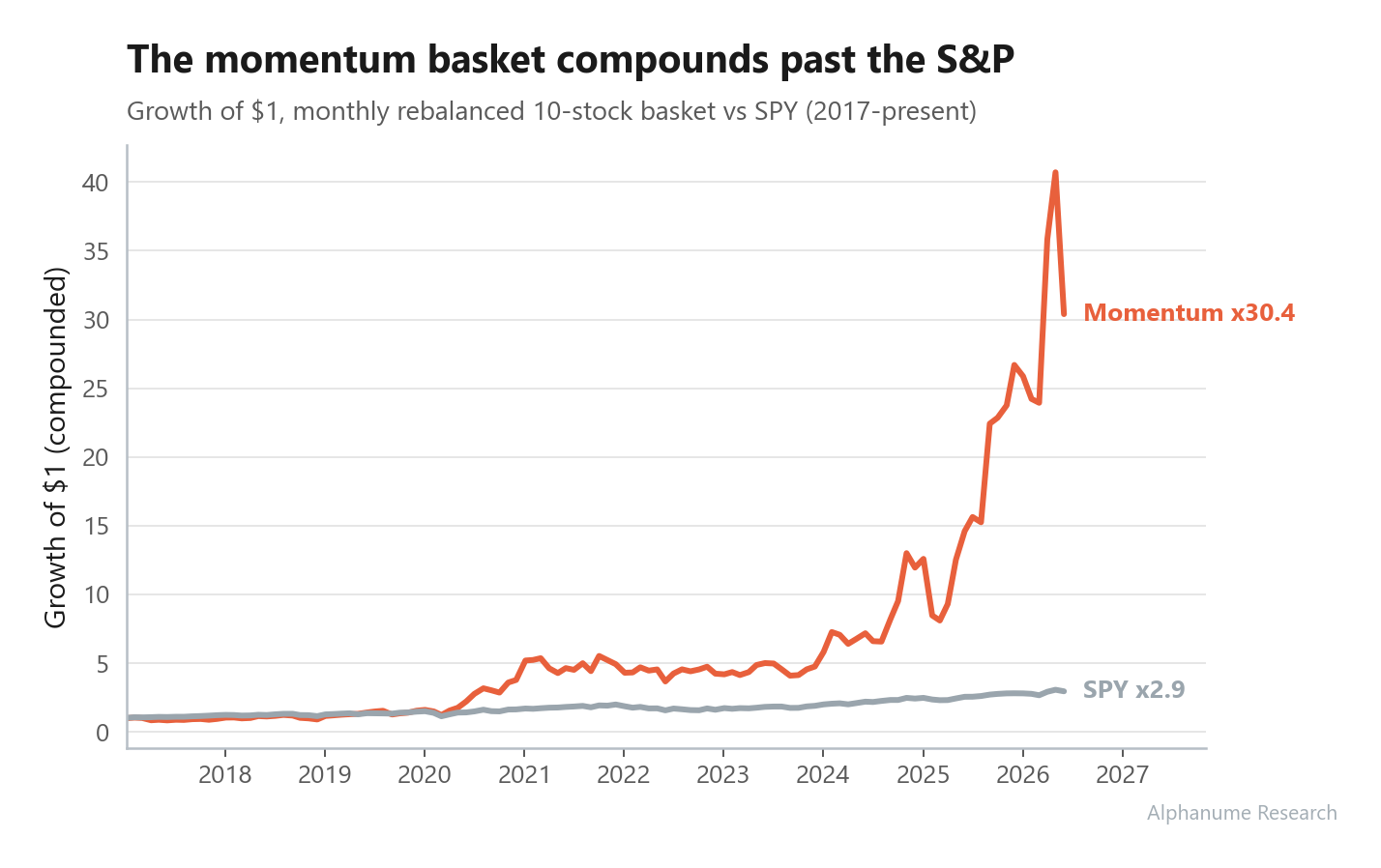

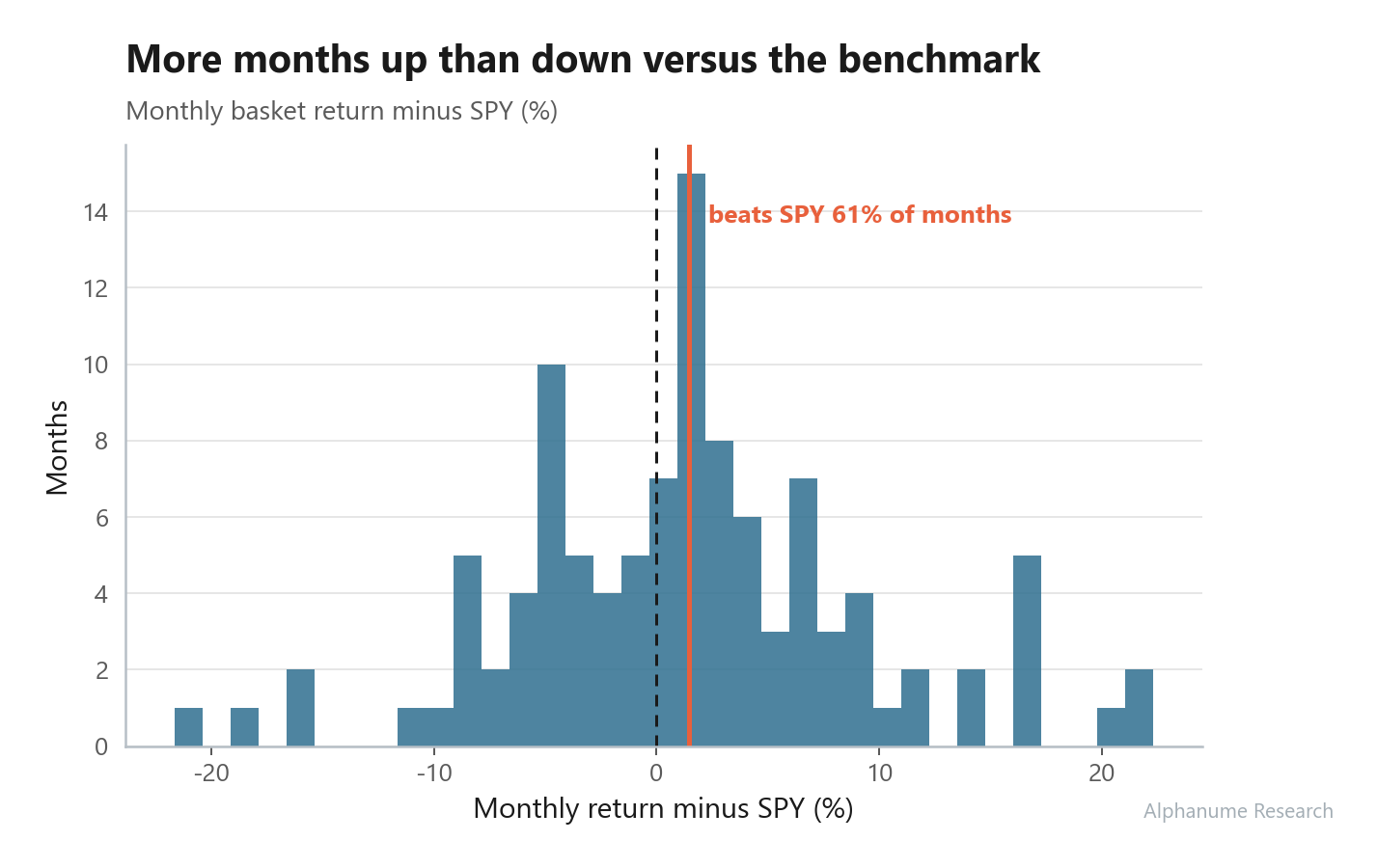

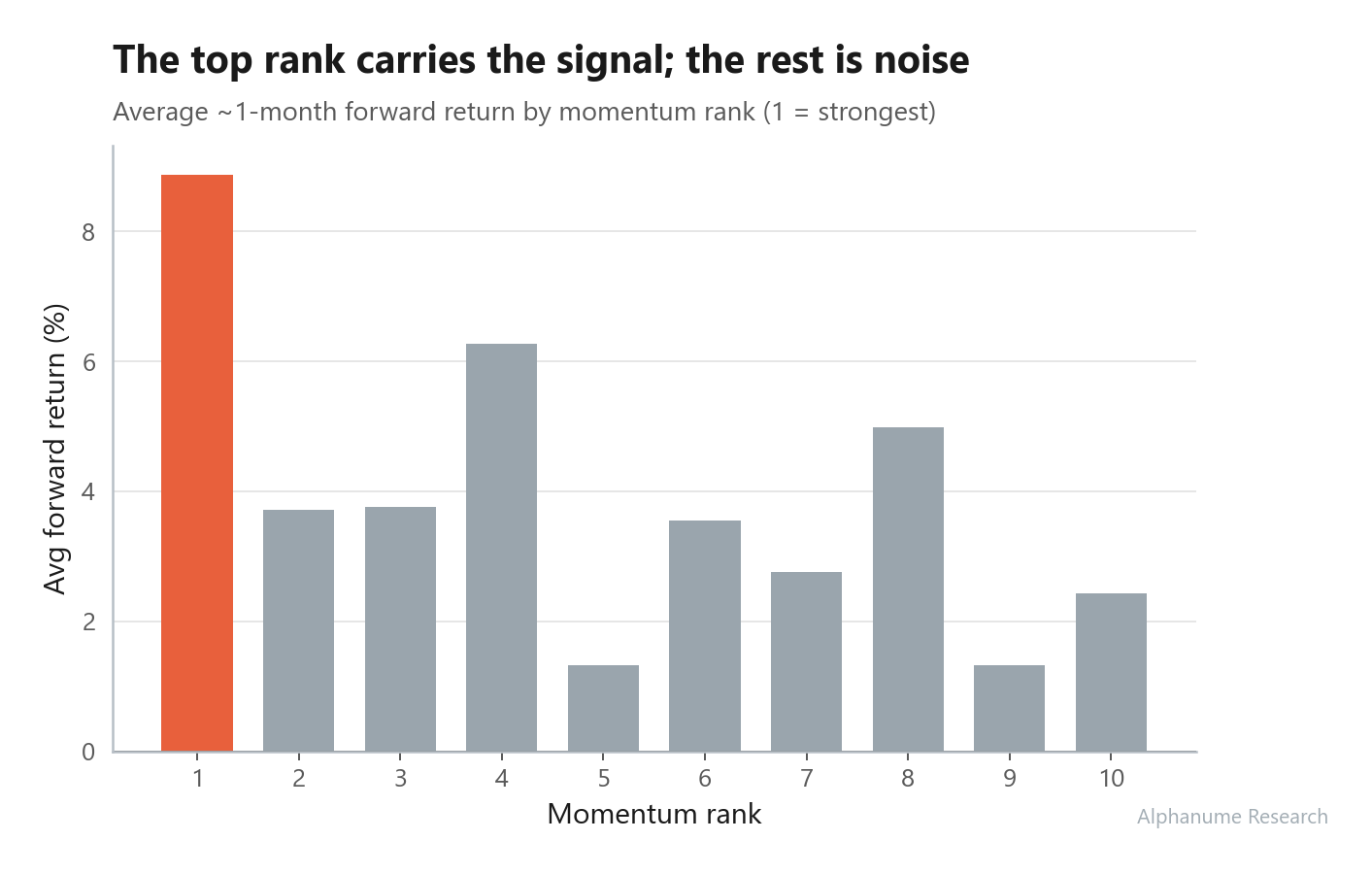

Quant Galore Momentum Index

114 monthly rebalances, 208 names · Jan 2017–presentA rules-based, 10-stock, monthly-rebalanced cross-sectional momentum basket. It compounds far past the benchmark: real, significant outperformance, but high-beta momentum risk, not a smooth ride.

$1 grows to $30.4 vs. $2.9 for SPY since 2017; beats the benchmark 61% of months, +2.84% mean monthly excess (t = 2.7).

08.1Compounded equity curve vs. SPY

08.2Monthly excess-return distribution

08.3Forward return by momentum rank

IV/HV Premium

294,503 settled rows · 2024–presentPer name and day, implied vol measured against realized, as a spread and a ratio. A conditioner: it tells you when implied is genuinely rich, which is the one regime where selling vol pays (selling blindly in this universe loses).

Seller edge sorts monotonically -9.4 to +5.1 vol points across IV/HV-ratio quintiles (14.5-pt long-short spread); win rate 27% to 53%.

09.1Seller edge by IV/HV quintile

09.2Seller win rate by quintile

09.3Edge distribution, richest vs. cheapest

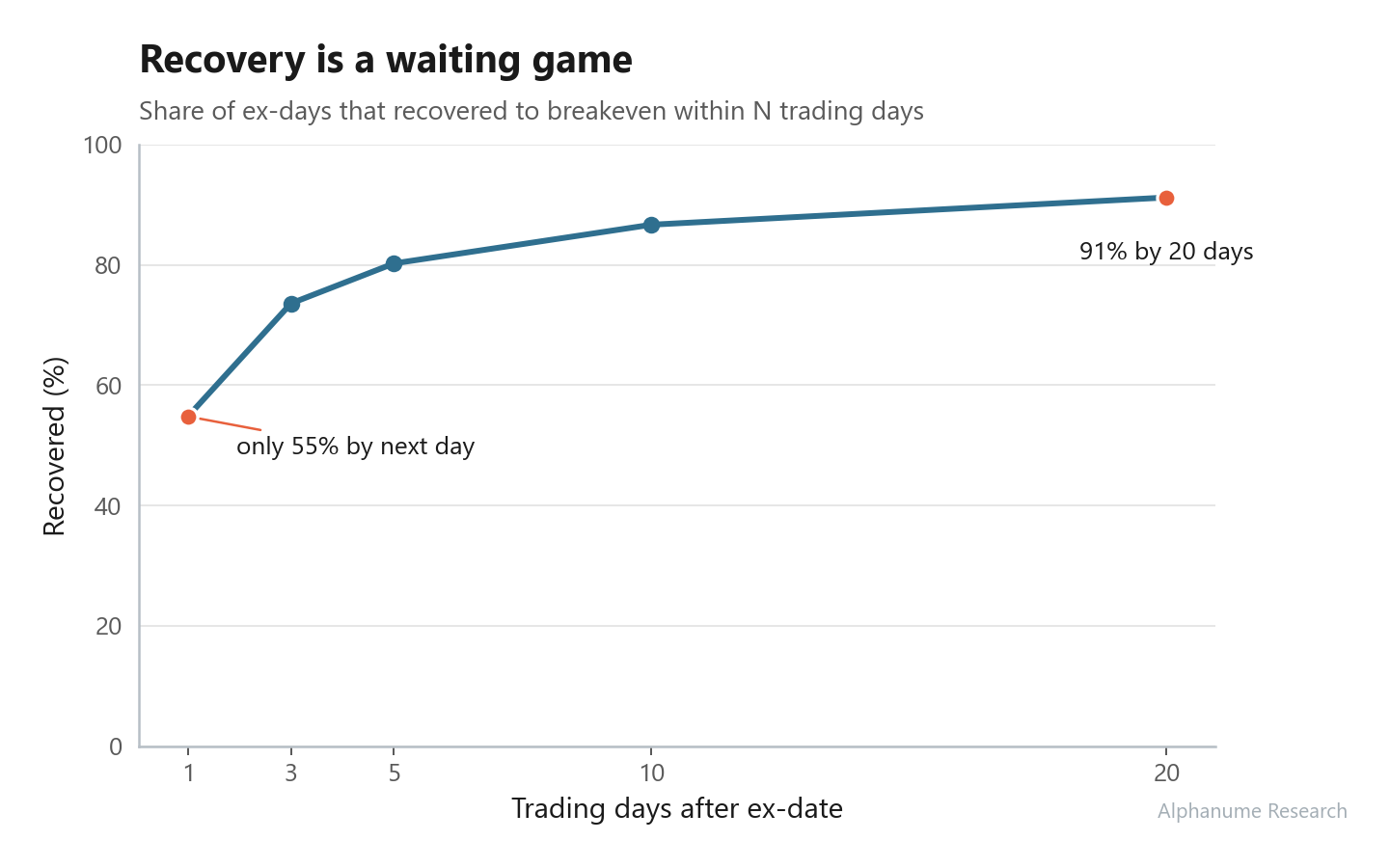

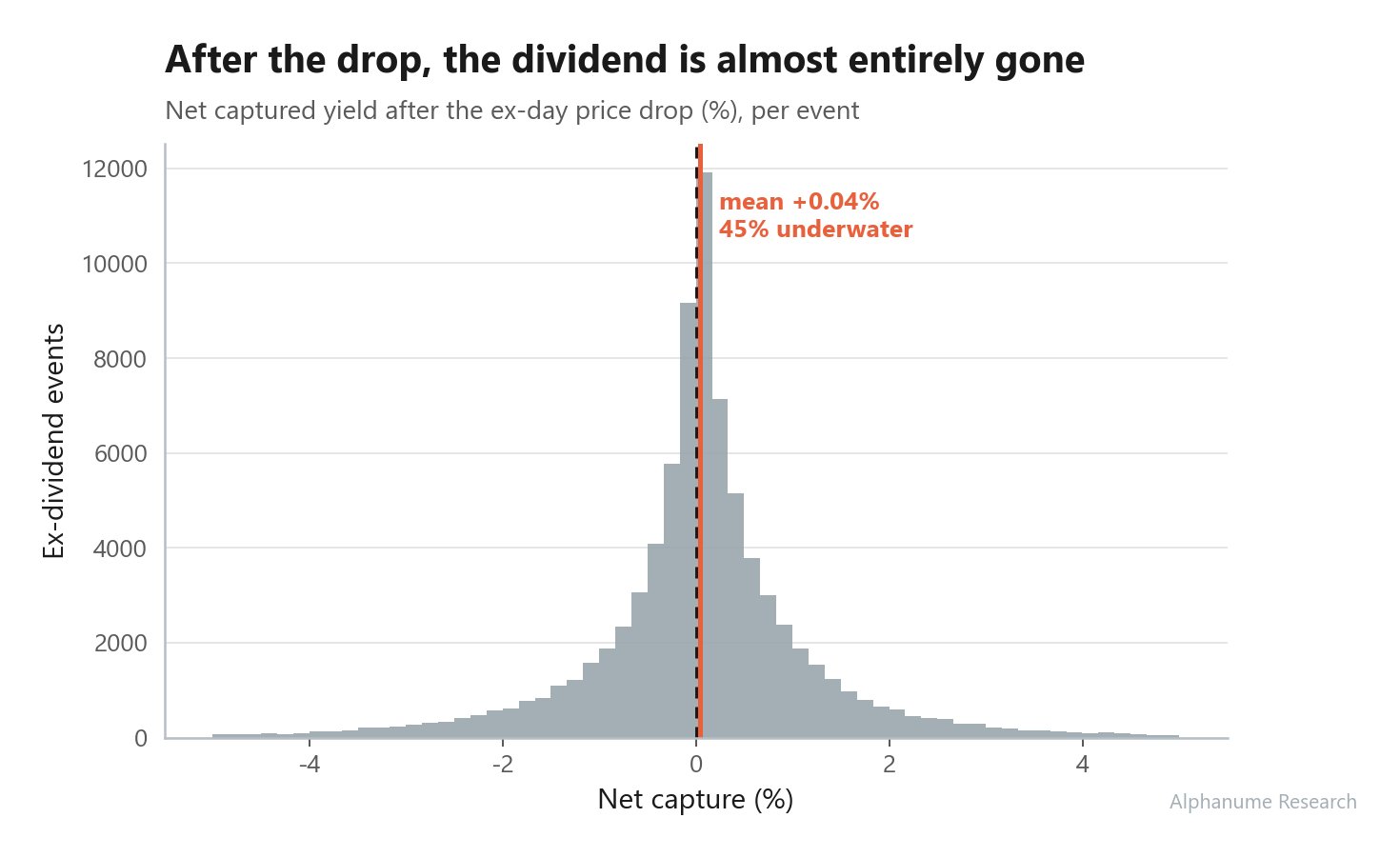

Dividend Capture

82,012 resolved ex-dividend events · 2024–presentEx-dividend events with drop ratios, net capture, and recovery odds. The mechanical claims hold tightly, and that is the alpha: the dataset lets you avoid a trade that looks like free yield but is near-zero EV.

Ex-day drop averages 0.87x the dividend; net capture is +0.04% with 45% of events underwater; recovery 55% (1d) to 91% (20d).

10.1Ex-day drop ratio distribution

10.2Recovery odds by horizon

10.3Net capture distribution

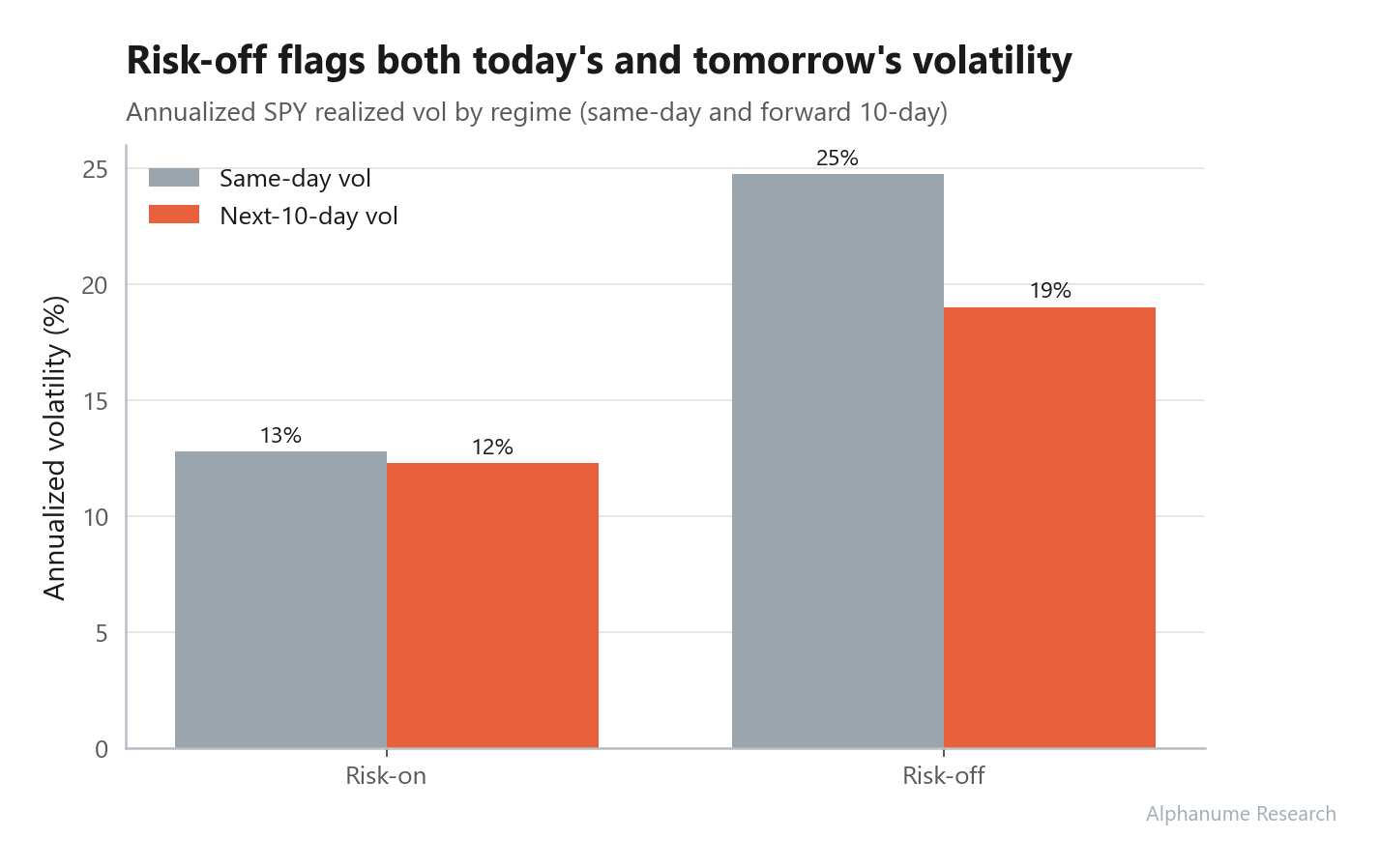

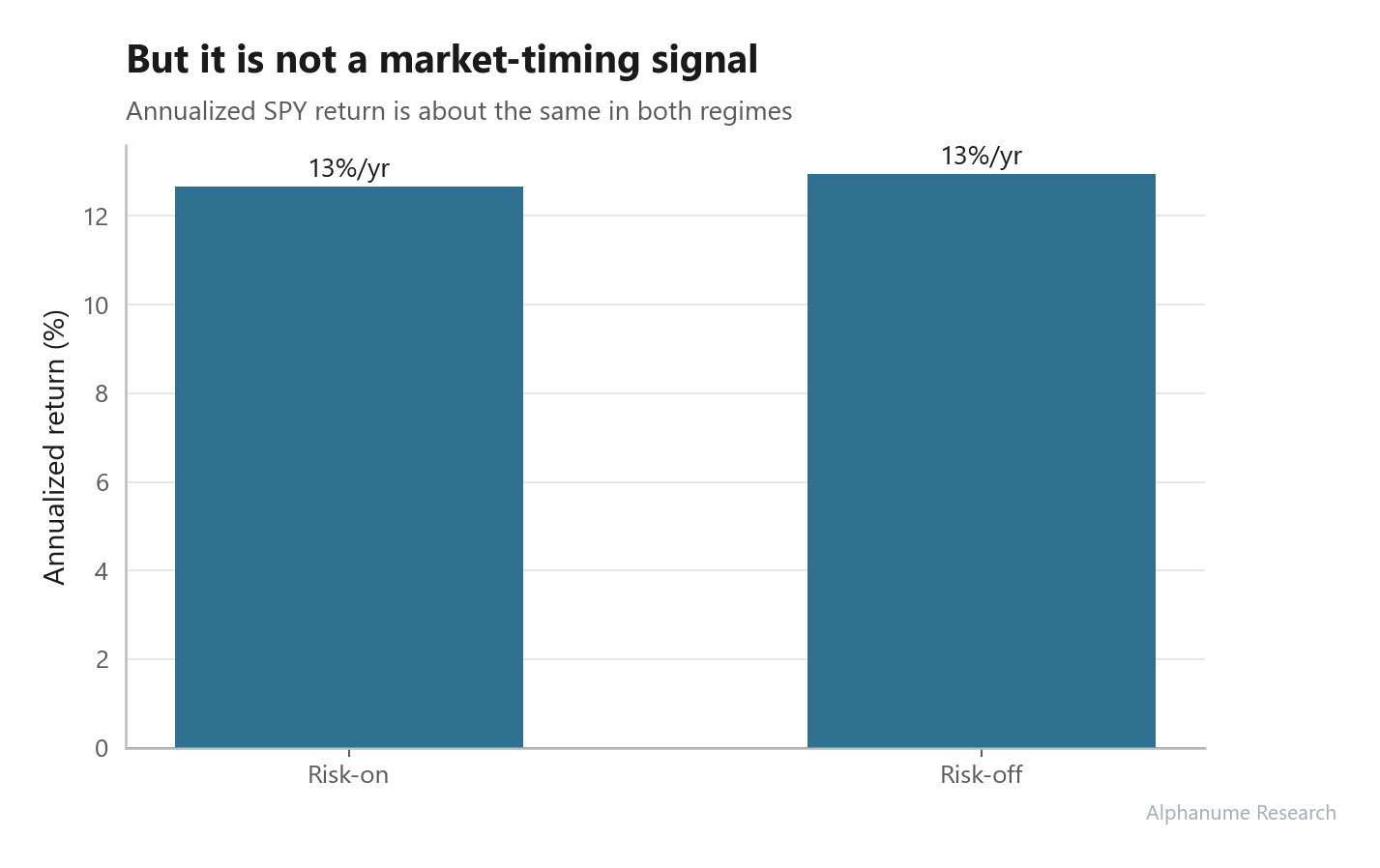

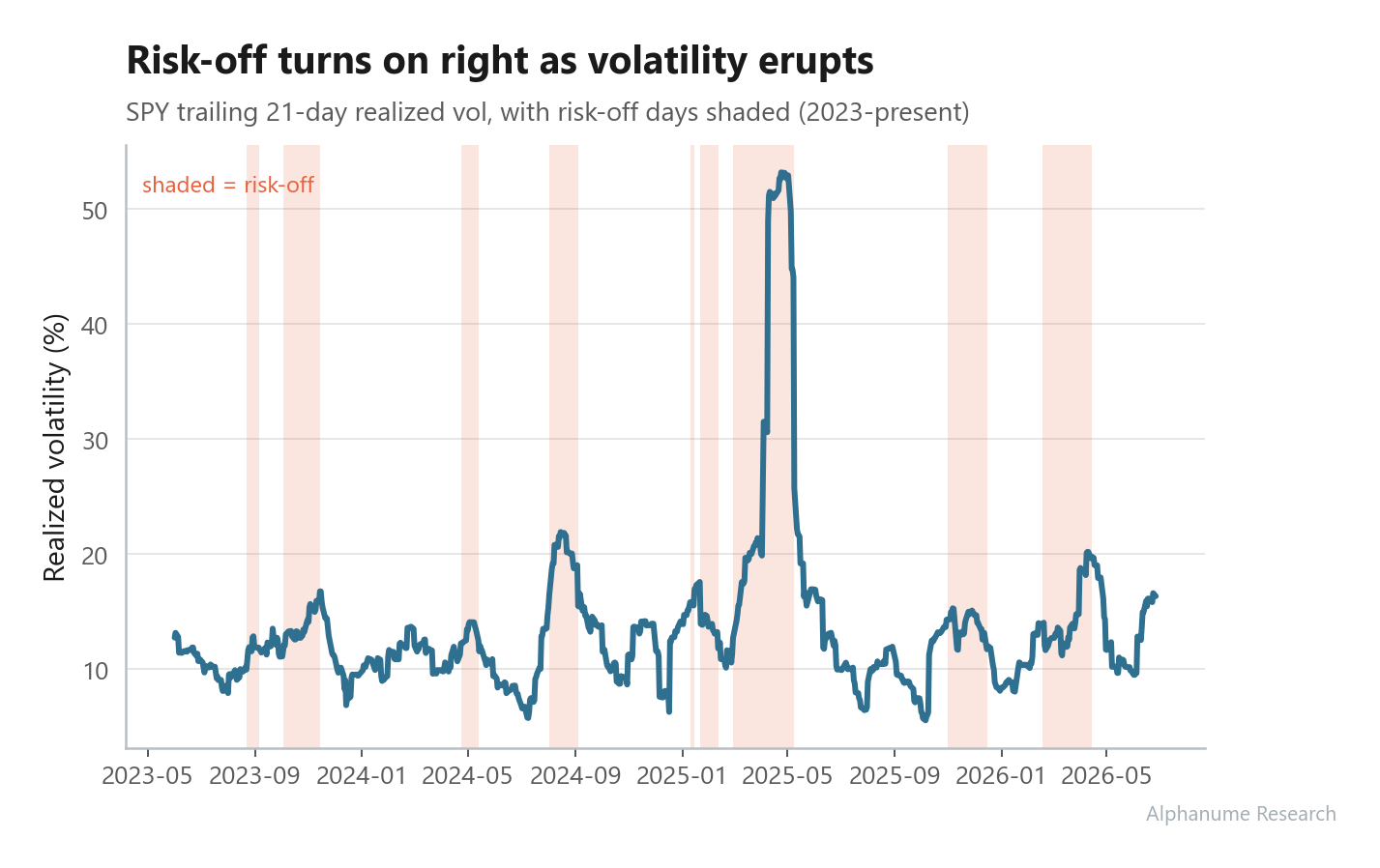

S&P 500 Risk Regime

3,833 trading days joined to SPY · 2011–presentA daily risk-on / risk-off flag. Read honestly: it is a strong, forward-looking volatility signal for sizing exposure and timing vol trades, not a market-direction call. Returns are the same in both regimes, and we show the flat chart deliberately.

Risk-off days realize 24.7% vol vs. 12.8% (2x); forward 10-day vol 19.0% vs. 12.3% (t = 15.0). Returns: 13.0% vs. 12.7%, not directional.

11.1Realized vol by regime, same-day and forward

11.2Returns are not directional

11.3Risk-off days shaded over realized vol

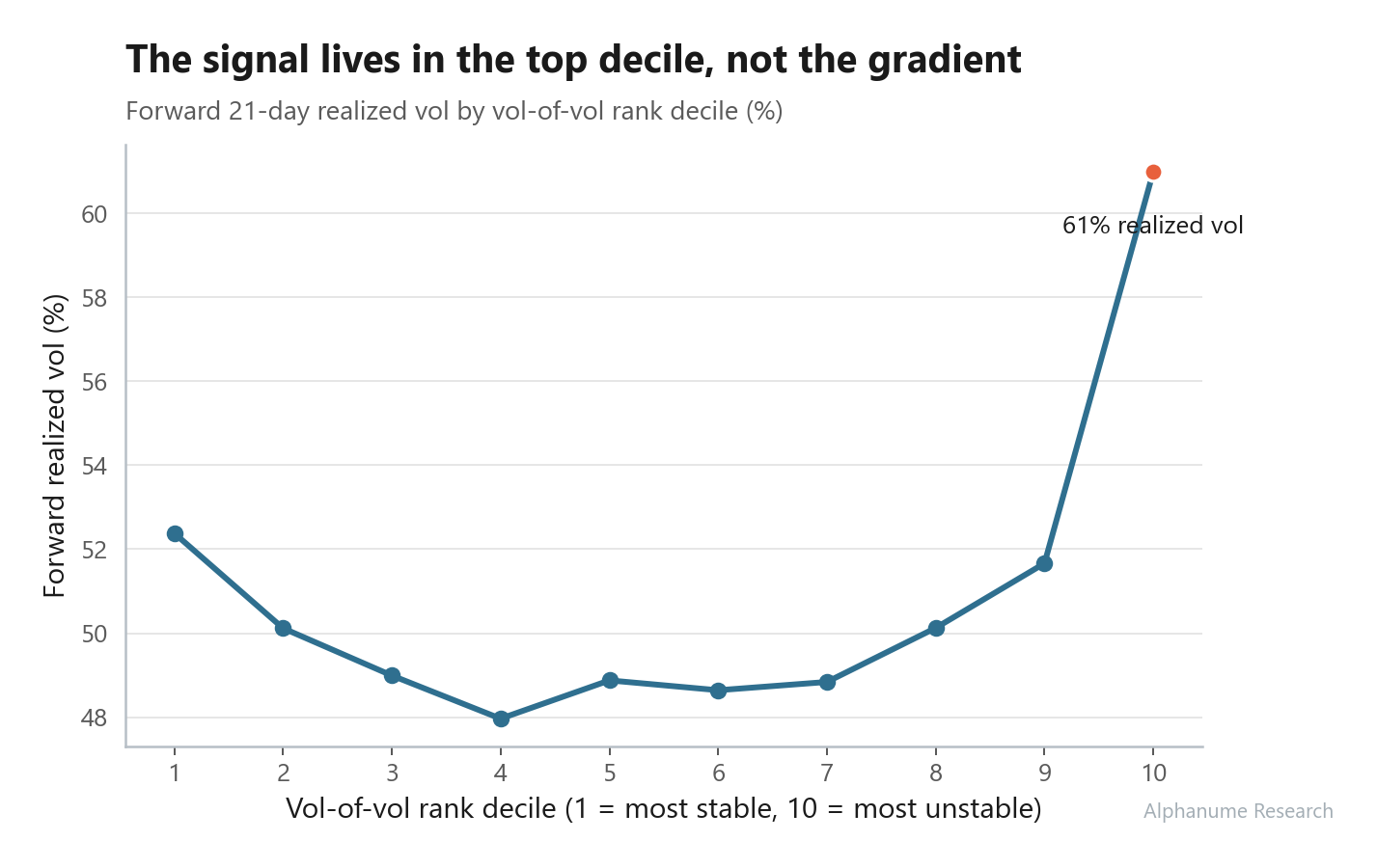

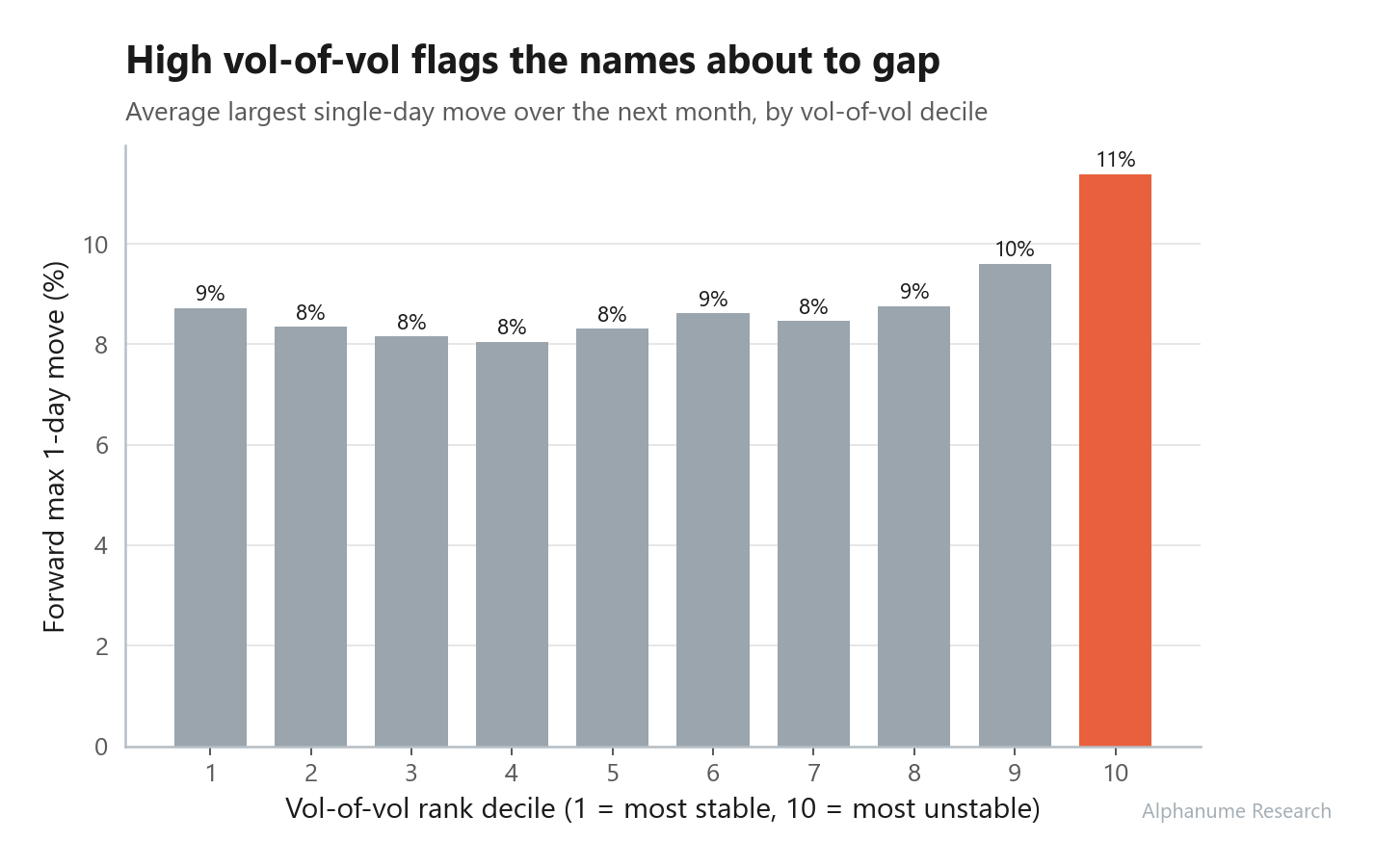

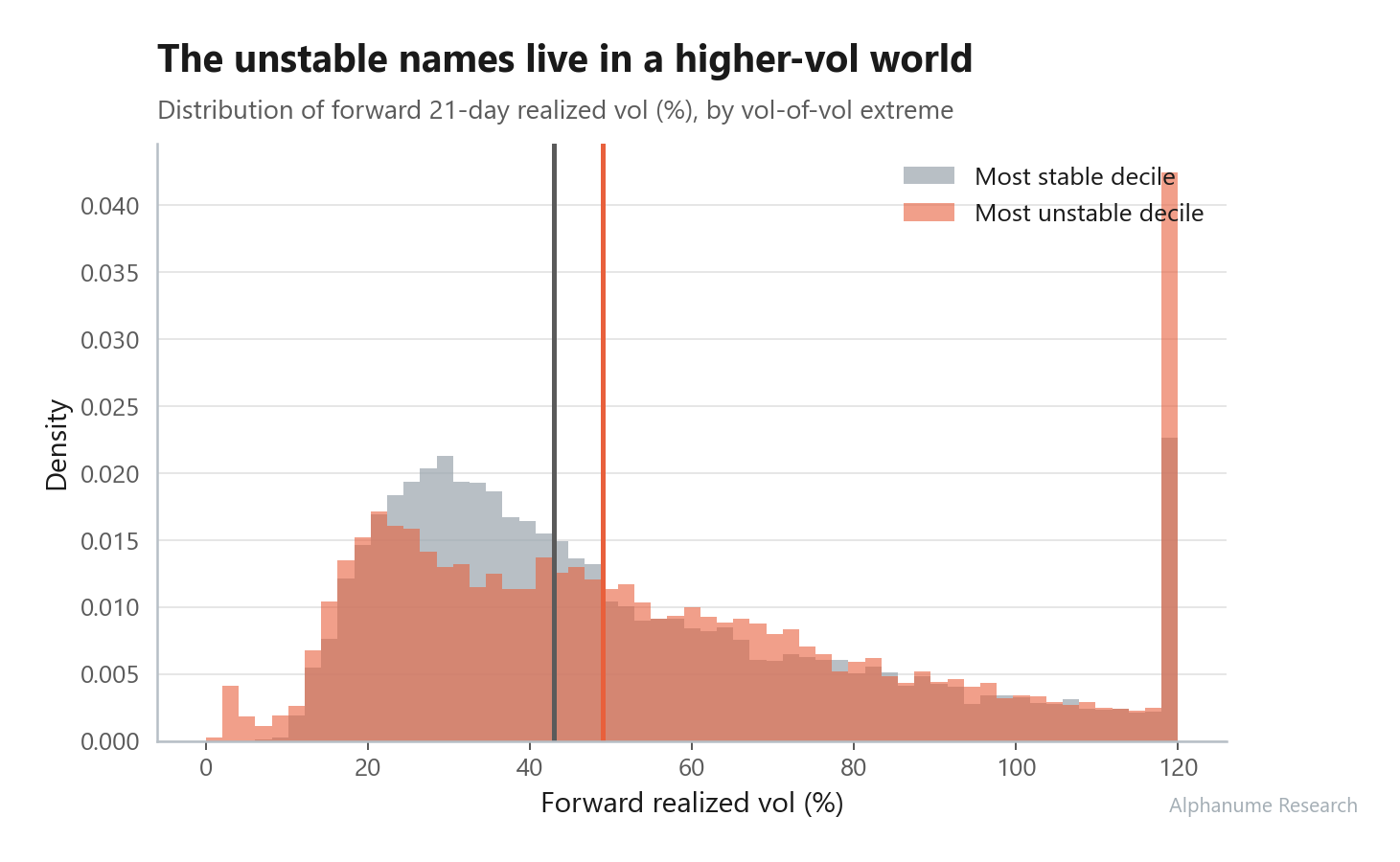

Vol-of-Vol Index

280,105 settled rows · 2024–presentHow unstable a name's volatility has been over the trailing month. The weakest signal in the suite, reported as such: it is not a clean cross-sectional factor; it earns its keep only as a top-decile tail flag.

Correlation with forward vol is just 0.05 and non-monotonic. At the extreme it works: the top decile realizes 61% vol and 11% max moves vs. ~8% elsewhere.

12.1Forward realized vol by vol-of-vol decile

12.2Forward max single-day move by decile

12.3Forward vol distribution, unstable vs. stable

The evidence is on the page. The data is one query away.

Every result above is reproducible against the same point-in-time observations a live strategy would see. Browse the full index, read the methodology, or open an account to pull the data through the REST API.